In private equity real estate investing, the capital stack refers to the organization and hierarchy of all the capital contributed to financing a deal. Investors must understand the capital structure of a private real estate investment, along with the risks and rewards associated with every position in the capital stack, before investing.

The investor’s position in the capital stack determines at what point they would receive the income and profits generated by the property throughout the hold period and upon sale. More importantly, it also determines how legally and financially responsible an investor would be if the property underperformed or in the event of a bankruptcy.

The stack is divided into two large categories – debt and equity. The lower down on the capital stack, the lower the risk and lower rate of expected return an investor receives, and vice versa as one moves up the stack. However, the keyword used here is expected, because ultimately one never knows how a deal is going to turn out. A debt investor could actually receive higher returns than an equity investor. For example, if an asset loses value upon selling, debt is contractually obligated to be paid back, whereas equity investors would be the first to lose money.

Senior Debt and Mezzanine Debt

Debt is at the bottom of the capital stack and involves lending money for the property’s acquisition or development. Less risk is involved at this position of the capital structure because these investors receive contractual interest payments, regardless of the property’s performance, and they are the first to be paid when the property is sold. Just like when an individual defaults on a home mortgage, if a deal goes into default, the lenders get to seize the building via foreclosure. This is the lower risk, lower reward position. Debt can be broken down further into two categories: senior and mezzanine.

At the very bottom of the capital stack lies senior debt, which typically takes up the majority of the stack. It is generally a mortgage secured by the property itself, meaning the asset can’t be sold unless the mortgage is paid. It is considered the least risky position due to its security interest in the property, which means senior debt holders receive ongoing interest payments and will be paid back first upon sale. While it’s the safest position in the capital structure, it also delivers the lowest expected returns to investors in exchange for having this first access to cash flows.

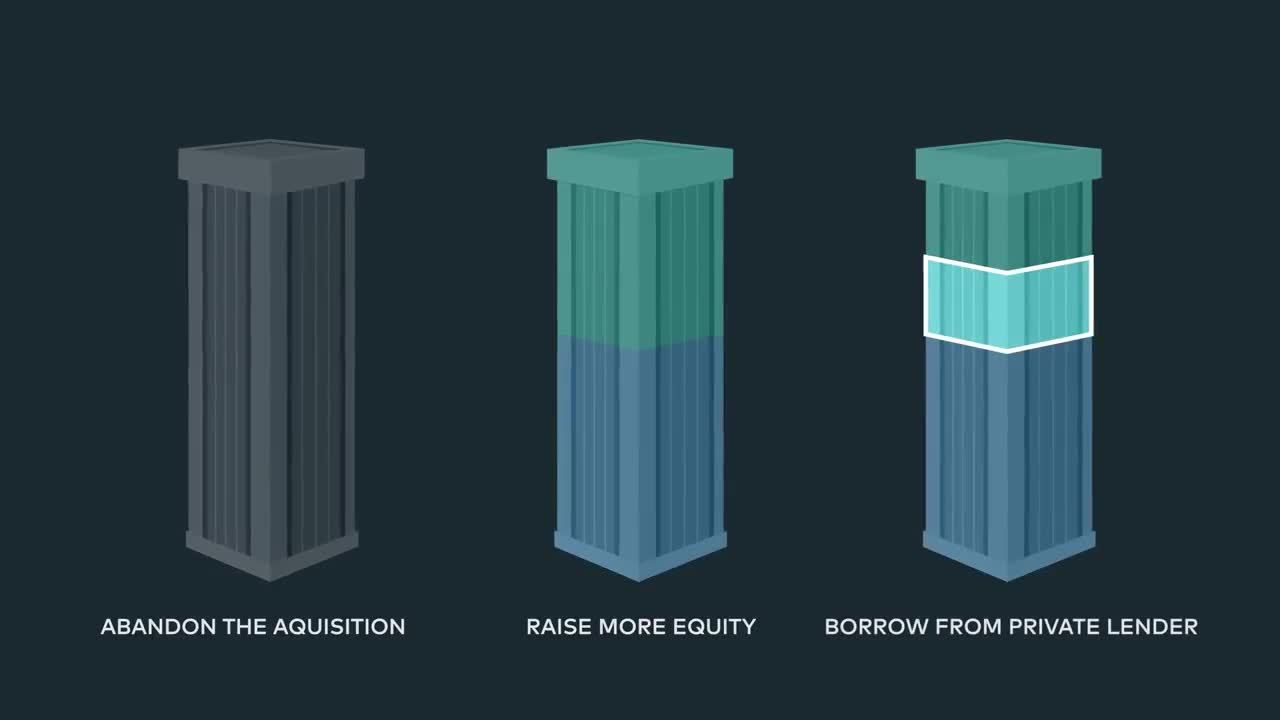

Mezzanine debt comes after senior debt in order of payment priority. Mezzanine debt investors receive a higher rate of expected return than senior debt investors because they will only get paid once all senior debt obligations have been made. Like with senior debt, mezzanine debt investors receive periodic interest payments. Mezzanine debt investors receive a lower rate of expected return than those in equity positions because their position is also secured by a junior mortgage or pledge of equity in the borrower. Not all deals allow mezzanine debt. The senior lender reviews and approves all mezzanine debt investors.

The upside of lending money to real estate deals is that investors receive a steady stream of cash from monthly debt payments, but the downside is that there are no tax benefits, as the income is taxed as ordinary income. A risk of debt investing is inflation, which lowers the purchasing power of those monthly cash streams because they’re fixed. In other words, if inflation rises from 1 to 3 percent, lenders will still get paid the same amount and that money won’t get them as far. Another downside of debt investing is that if the deal outperforms the lenders do not share in the additional profits.

How a mezzanine loan bridges the gap between equity and debt in a capital stack.

Common Equity and Preferred Equity

Equity is at the top of the capital stack and involves ownership. It is the riskiest position of the capital structure as equity investors are paid last. Because of this, individuals require the largest expected returns to compensate for that risk. This is the higher risk, higher reward position. Equity can be broken down further into two categories: common and preferred.

Preferred equity is a hybrid position that sits between equity and debt in the capital stack. It’s senior to traditional equity investments but subordinate to debt positions. Like debt investors, preferred equity investors receive contractual payments throughout their investment period and generally don’t participate in any additional profits the investment generates. However, they should receive a higher expected return than debt investors because their investment is unsecured.

Common equity is at the highest position of the capital stack, which contains the most risk, but investors also have the most to potentially gain for this risk. Being a common equity investor means being an owner of the deal. It is the riskiest position of the capital stack because investors are only paid back after all the other positions in the capital stack have been repaid. However, common equity investors will receive all the profit upon the asset’s sale.

Common equity investors also receive the benefits of the full appreciation of the asset; buying low and selling high makes common equity holders, not debt holders, money. Since common equity investors are owners of the asset there is no fixed term for their investment and their full payout happens only when the property is sold or when an investor sells their ownership interest. In the simplest terms, when things go well with an investment, all the investors win, but the equity investors win more. When things go poorly, equity investors are the last to get paid back. Equity investors also receive the tax shield benefits of depreciation and have the right to defer their tax gains into their next investment.

How We Position Ourselves within the Capital Stack

At Origin, we positioned ourselves at the top of the capital stack for our last three funds – Origin Fund I, II and III. In those funds, we executed on nearly $1 billion of transactions with zero losses and were cited as a consistent top-performing private real estate manager by Preqin, a research company that provides financial data and information on the alternative assets market.

At the start of 2019, we launched our IncomePlus Fund, which targets both debt and equity multifamily investments in 10 of the nation’s fastest-growing markets. With this fund, we aim to create the same amount of wealth as our previous three funds, but at a lower risk level. Unlike our other funds, approximately 25 percent of the IncomePlus Fund will consist of preferred equity and mezzanine debt and the remaining 75 percent will be in equity positions. We believe this structure will provide investors with the tax benefits of common equity, but with the lower risk of preferred equity.

Why Understanding the Capital Stack Matters

Every real estate investment is unique, with varied capital structures, offering their own potential risks and expected returns. Before investing, it’s crucial to be informed about every position in the capital stack for every individual opportunity. Investors should allocate their capital between equity and debt investments based on their risk tolerance and investment goals. If you are more tolerant of risk, then having more real estate equity investments in your portfolio may be more appealing and could better satisfy your investment goals. The opposite can be said for risk-averse investors who may be more attracted to real estate debt investments, as they may be less risky.