What is a good investing decision? What is a bad investing decision? Is the decision defined by the outcome or is the outcome defined by the decision? Would you rather make a good investing decision where you lose money or a bad investing decision where you make money? While the answer to this may seem rhetorical, it is definitely not.

Humans are irrational beings who rationalize decisions. Most decisions are made subconsciously in the oldest part of the brain, the reptilian brain, responsible for fight or flight, and are rationalized in the part of the brain responsible for cognitive thinking, the neocortex. The reptilian brain drives decisions far more often than the neocortex. The reptilian brain is where human bias comes into play, which can only be limited by adhering to rigorous processes designed to focus on facts.

For example, most real estate investors would choose to invest in a brand new beautiful high rise rather than an old beat up apartment building well before they analyzed the underlying data. This is because emotional responses in the reptilian brain lead to impulsive decisions and we are wired to like bright and shiny objects. These decisions are later rationalized in the neocortex, but data is intentionally ignored because the decision has already been made. We essentially make up our mind without even knowing it.

Subscribe

Subscribe to receive the latest articles about fund updates, industry news and market trends.

Here’s why that matters:

Whenever we make a decision, there is always an associated outcome with that decision. In the world of investing, this is called the expected return. When we make an investment and take on a certain amount of risk, we expect to be compensated adequately for that risk. If I flip a coin ten times, I expect that it will land on heads half the time and tails half the time. However, the actual investment outcome is often far different from what we expected, which means we can experience significant variance around the expected outcome.

It may be that flipping the coin ten times results in heads eight times and tails only twice. The goal is to keep flipping the coin, so the law of large numbers prevails. If I flip the coin 1,000 times, the odds are heavily in my favor that it will land on heads and tails an equal number of times. This concept helped to build every casino around the world and can also be applied to investing.

Whether a decision is good or bad is defined by the probability of the outcome, not the outcome itself. If you make a decision and reasonably expect it to yield a positive result eight out of ten times, then it’s a good decision, such as making a long-term investment in the S&P 500. On the flipside, taking your life savings and heading to Vegas to play blackjack in the hopes of doubling your money is always a bad decision.

Investing is about making sure the odds are in your favor to win over the long run. We like to think that good decisions lead to favorable outcomes and bad decisions lead to poor outcomes, but it’s just not that simple. In the world of investing, reckless behavior can sometimes be rewarded with financial gain while prudent conservative investing can lead to a loss. Human bias impacts the decisions we make, and the process of bad decision making can be reinforced by a positive outcome. We tend to think that the same decision in the future will lead to a similar outcome, but the reality is that we simply got lucky.

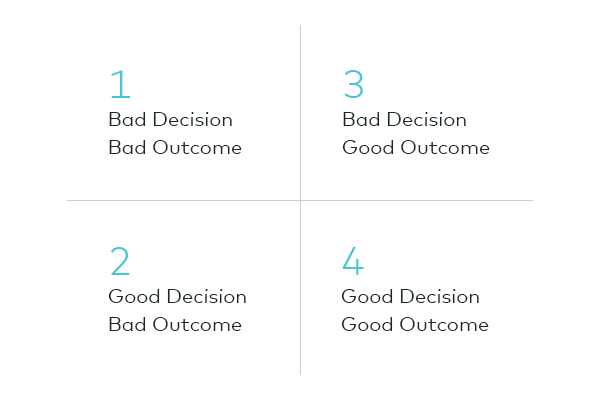

Matrix of Decisions and Their Associated Possible Outcomes

The matrix below illustrates the four quadrants of possible outcomes related to various decisions. Every investor has spent time in each one of them but it’s quadrant four where wealthy investors and those who want to be wealthy should focus. This is the quadrant that will yield the greatest wealth over time because the more good decisions we make, the more likely we will be successful in the long run.

Let’s evaluate each one of these in depth to better understand the ramifications of operating inside them.

Quadrant 1 – Bad Decision/Bad Outcome

This is the quadrant defined as the ‘What was I thinking?’ quadrant. It’s also known as the learning quadrant because of the valuable lessons gained and because these lessons can be more expensive than an MBA. In this quadrant, a bad decision leads to a bad outcome.

Anyone who has invested long enough has operated in this quadrant once or twice. These are the bright and shiny deals that jump out and sound fun. Maybe you decided to take a flyer on a penny stock, made an investment with a now-bankrupt real estate developer, were lured by the potential of a 40% return, or invested in an upscale sock company. Making these mistakes early in your investing career is a good thing when the stakes are low, but you want to exit this quadrant as quickly as possible. These are the learning experiences that make us better investors.

Bad decisions can also be about the investments you don’t do. Great investments aren’t easy to find and letting the good ones go can be painful, especially if that money is later invested in a deal that was less promising. Again, it’s about the probability of success or failure that matters. There are many real estate deals we’ve passed on at Origin that have performed well, but we wouldn’t make a different decision if we came across the opportunity again.

For example, investing with an inexperienced and undercapitalized operator in a pioneering location where they want half of the returns is not a good risk/reward scenario. It’s also the deals we passed on for the wrong reasons that create those painful learning experiences. There are no mulligans in investing so all we can do is the draw from that past experience when we are faced with a similar situation in the future.

Quadrant 2 – Good Decision/Bad Outcome

This is the quadrant defined as “What went wrong?” You reflect on your decision and look for ways in which you could have made a better decision, but you would have made that same decision again under the same circumstances. Eight out of ten times you would have made money but in this case, it didn’t happen.

No one is immune to landing in this quadrant, including Origin. For example, in 2011 we acquired a student housing project in Tallahassee, Florida. It was well located, came with a free large parking garage, and we bought it 40% below replacement cost. Those facts made it a compelling investment. Fast forward one year and suddenly supply issues started to emerge, school enrollment was declining, rental rates were falling, and our operational partner couldn’t manage the challenges. In this case, every potential risk we identified came to fruition. We ended up cutting our losses and selling the property after 14 months.

At Origin, we will buy hundreds of properties over the next ten years and we strive to continually improve our decision-making process. If we pass on an asset for the right reasons, we don’t look in the rearview mirror. It might be that the deal came with too much leverage, an inexperienced partner, complex issues that didn’t justify the returns, an inferior location or problems that we simply couldn’t solve.

Quadrant 3 – Bad Decision/Good Outcome

This is the most dangerous quadrant. Staying in this quadrant for an extended period of time is the quickest way to utter the five most feared words, “I used to be rich!” As Bill Gates once stated so elegantly, “Success is a lousy teacher. It seduces smart people into thinking they can’t lose.”

Unlike the lucky person in the first quadrant who lost money when they made a bad decision, the investor in this third quadrant had a favorable outcome. And generally, when something feels good, we repeat that behavior but with bigger stakes. Instead of learning a lesson and getting out of the habit of making stupid investment decisions, this investor is emboldened by the outcome. They don’t realize that their decision is one that would lose money eight out of ten times.

Everyone knows a story of a successful person going broke because of reckless investment behavior. Unfortunately, it’s all too easy to get trapped in this quadrant because these investments tend to emotionally entice us. Who doesn’t want to own an island, be part of the latest social media app, or potentially make 10 times their money? The fear of missing out on the next great idea is a powerful motivator that can easily influence decisions and drain bank accounts.

This is the quadrant of so many lessons. Check your ego. Know what you don’t know. Don’t put all your eggs in one basket. Don’t pour good money after bad investments. Diversify your portfolio. You only have to get rich once.

The bankruptcy of Curt Schilling might be one of the most highlighted examples of reckless investing. Curt is a former Major League Baseball pitching phenom who is destined for the hall of fame. He made more than $90 million in career earnings and sunk it all into a gaming company that ultimately failed. Curt’s early success in baseball led him to believe he couldn’t lose in a completely different industry.

Quadrant 4 – Good Decision/Good Outcome

This is the quadrant where we all want to spend the most time. Nothing is better than when a well thought out decision leads to the outcome you expected. The problem with this quadrant for most people is that it’s boring. And boring isn’t an emotion that does well in the reptilian brain. But the reality is that diversifying your portfolio and earning 7% annually is the best way to ensure long term wealth.

What is the likelihood that your investment portfolio will be worth eight times what it is today in 30 years? Would you settle for this? Most people answer this question yes, but then their investing behavior differs radically from what they are trying to achieve. A 7% return over 30 years will multiply your investment eight times over when you consider the power of compounding.

We have many examples in the Origin portfolios that can be used here. As a firm, our goal is to make sure we operate in this quadrant at all times. We constantly evaluate our decision-making process and work to refine it where we can. We reflect on deals we didn’t do, evaluate deals that went better or worse than expected, and use our experience to make the best choices we can. We won’t get every one of them right, but we will get most of them right. And our decisions are not limited to just deals. Who we hire, how we deploy resources, where we look for investments and even being in real estate are all conscious decisions designed to produce a better outcome.

The views expressed herein are exclusively those of Michael Episcope, are not meant as investment advice and are subject to change. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this article.