The only thing that matters when evaluating an investment is what you put in your pocket after all fees and taxes are paid. Many investors fail to realize that comparing investments on a pre-tax basis only makes sense if you are investing non-taxable money. It might be very appealing to consider a hedge fund that targets 20% returns, but those returns don’t look nearly as shiny when the government takes 37% of your profits. Also, a stable debt investment that yields 8% doesn’t fare much better than a municipal bond once the tax bill is paid. Individual investors must consider the impact of taxes when comparing investment opportunities and look for investments that are tax efficient.

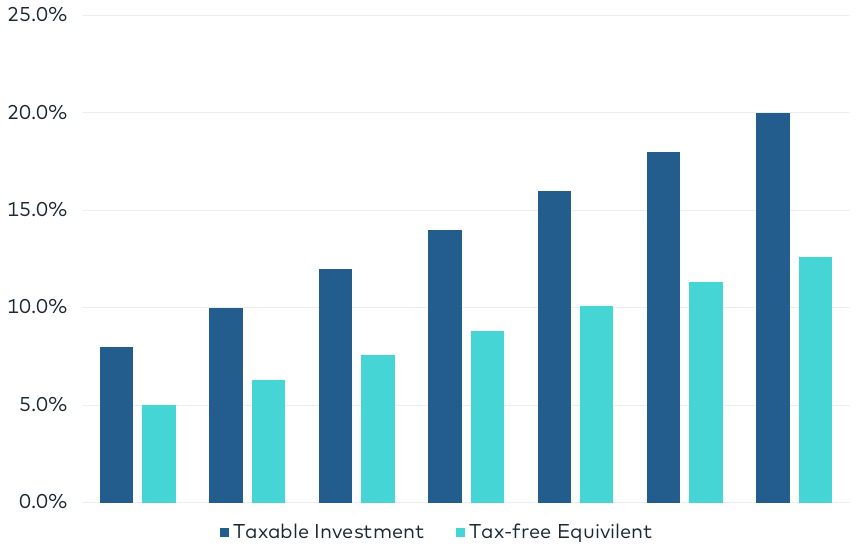

Having an investment that generates an 8% cash yield is great, but a 6% yield on a more efficient investment might actually be better on an after-tax basis. The chart below shows the after-tax return of investments based on a 37% tax rate. An 8% pre-tax return only generates about a 5% after-tax return.

Private real estate has long been known as one of the most tax efficient investments with the ability to shield income through depreciation, return capital tax-free through refinancing, and defer capital gains indefinitely through 1031 exchange sales. However, most private equity real estate firms, including Origin, don’t take advantage of these tax benefits because they utilize a buy, fix, and then sell strategy. The short asset hold periods don’t allow companies to take advantage of depreciation and refinancing and each sale triggers a taxable event.

The desire to deliver the most efficient after-tax risk-adjusted return is the exact reason why we created the Origin IncomePlus Fund. The “buy, fix, and hold” strategy allows investors to maximize the benefits from owning real estate for the long haul; tax shields, tax-free refinancing, and deferring gains indefinitely. Investing in this manner also means we can take less risk and generate more wealth over the long run.

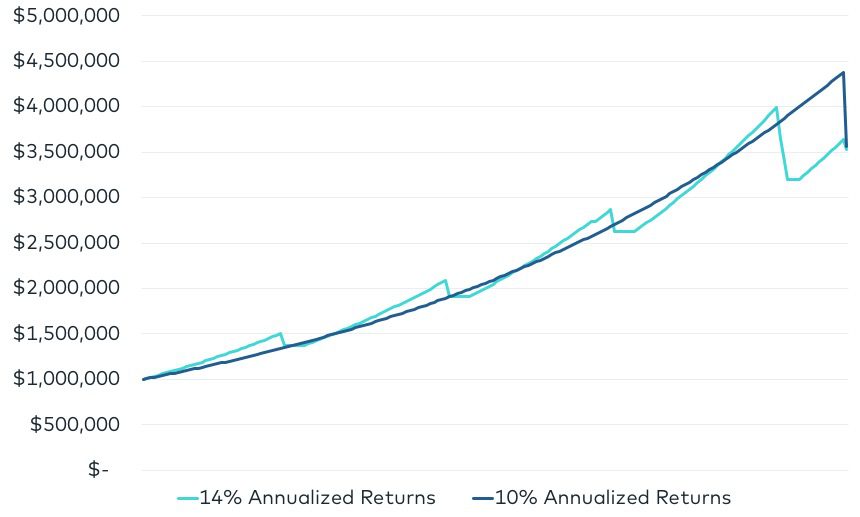

The fact is that a tax-efficient investment earning 10% returns annually will get you to a similar place as an inefficient taxable investment earning 14% returns. The chart below illustrates this point.

The line in light blue represents the growth of $1 million invested over three-year periods earning a 14% annualized return in each period. The dip in the light blue line represents a conservative impact of taxes and six months of cash drag as the money isn’t earning anything while you look for another opportunity to redeploy the capital. In many cases, a distribution that goes into one’s bank account never finds its way into another investment. The dark blue line represents that same $1 million earning 10% annually but invested in a tax efficient manner. In both cases, the end result is nearly the same and the relationship holds true whether the time horizon is five, 10, or 50 years. And, if you believe in market efficiency, the risk of an investment generating a 10% return should be far lower than the risk of an investment that generates 14% annually.

The illustration above uses a 30% tax rate but the gap begins to widen on investments such as debt and hedge funds which are taxed at roughly 37%, as the scenario below shows.

There are no tax-free investments that generate an annual return of 10% or more, but there are tax efficient and tax-inefficient investments. The friction of moving money in and out of investments must be considered in your overall investment strategy. The Origin IncomePlus Fund is a tax efficient investment designed to remove the friction of distributions and capital calls, and, with it, we intend to deliver the same amount of wealth as our previous funds, but with lower risk. There’s a reason why the famous investor, Warren Buffett, holds assets forever. He wants to avoid paying taxes and there is no tax on a stock or an asset until you sell it.

The views expressed herein are exclusively those of Michael Episcope, are not meant as investment advice and are subject to change. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this article. The calculations in this article assume a 14% internal rate of return versus a 10% annualized return. Both investments cited are held for 15 years and pay the equivalent tax rates, but the annualized investment defers it until the end of the investment period.