This article was originally published in December 2017.

A capitalization, or cap, rate is the ratio of a property’s net operating income (NOI) in the first year of ownership, divided by its purchase price. It’s a fundamental concept used in the world of commercial real estate. Investors who understand how a cap rate works and when to use it will gain deeper insights into potential investments.

How does a cap rate work? An asset with an NOI of $80,000 that costs $1 million has an 8% cap rate ($80,000 divided by $1,000,000). This formula also can be used in reverse to find a property’s market value. Let’s say a property has annual NOI of $60,000 and market cap rates are 6% for properties with similar characteristics. Then the value of the property would be $1 million ($60,000 divided by 0.06). This is a fairly simple definition. But it’s important to also understand how a cap rate is derived and its limitations in valuing real estate accurately.

Why does the cap rate formula work to value properties? It’s nearly identical to the formula used in finance to value a perpetuity (an income stream that runs forever). The formula is:

Perpetuity Value = Annual Income / Expected Rate of Return

To find the value of a perpetuity, take the annual income and divide it by the expected return. For example, an investor may expect to make 4% on an annual income stream of $1,000. So they would be willing to pay $25,000 ($1,000 divided by 0.04). We can also reverse the equation to determine the expected return at a given price. If the perpetuity is being offered at $30,000, then the expected return is 3.33% ($1,000 divided by $30,000).

Valuing a Property Using Cap Rates

Valuing a property using a cap rate works in the same manner. That’s because, in theory, property cash flows extend forever. In the formula above, NOI would replace the annual income (numerator) and the cap rate would replace the expected return (denominator). If a property is expected to produce $25,000 of NOI each year and market cap rates are 8%, then the property would be valued at $312,500 ($25,000 divided by 0.08).

A cap rate is actually a bit more complex than this example because we are dealing with fluctuating cash flows and a physical asset. Cap rates are a combination of two variables: expected returns and the growth rate of income. We explore both in greater depth below.

Capitalization Rate = Expected Returns – Growth Rate of Income

What is an Expected Return?

The expected return, also called the required rate of return, is the return the investor would expect to receive during the investment hold period. The riskier the investment, the higher rate of return an investor would expect. Expected returns are driven by the volatility and uncertainty of an income stream. That’s why stocks have a higher expected return than bonds. It’s also why an investor in a ground-up development apartment complex would expect to generate a higher return than an investor acquiring a stabilized apartment complex.

Expected returns change over time and are impacted by both the availability of alternative investment options and long-term bonds, the “risk-free” investment option. If an investor can generate 4% from a 10-year Treasury bond, then they certainly would expect a higher return from riskier assets. If an investor can achieve a 10% return from a stabilized apartment complex, they would expect to achieve a far greater return in a hotel development.

What Happens When Expected Returns Change?

Building on the perpetuity example above, if the required rate of return increases to 5% from 4% during the hold period, the value of the perpetuity will decrease to $20,000 ($1,000 divided by 0.05). Because the income streams are fixed, the only way for a new investor to get a higher rate of return is to pay a lower price.

The opposite also can happen when required rates of return decline. If the expected return declines to 3% from 4%, then the value of the perpetuity would increase to more than $33,000 (1,000 divided by 0.03). This is what happens to real estate values as cap rates decline. But a cap rate is more than just the investor’s expected return. It is a combination of both the expected return and the future growth of NOI, as real estate cash flows tend to increase over time.

Growth Rate of Income

NOI growth is one of the biggest advantages of owning real estate. Lease rates typically increase over time, providing owners with a growing income stream. Contractual rent growth is an agreement between lessee and lessor and is codified in a lease. Annual rent escalations are typically from 1% to 3%. Market rent growth can fluctuate between -5% and +10% in a market in any given year. But it typically averages from 2% to 4% in markets with robust jobs and population growth. Market rent growth is calculated by looking at the rental rates of newly signed leases on a year-over-year basis.

Growth of NOI is arguably the most important variable to consider when looking at cap rates. That’s because changes in growth assumptions can cause massive swings in a property’s value. In this case, growth refers to the expected future growth of income. Past growth matters only to the extent that it impacts people’s perceptions of future growth.

Here is the formula to value a growing perpetuity:

Perpetuity Value = Annual Dividend / (Expected Rate of Return – Future Growth Rate of NOI)

Building on the perpetuity example from above, let’s assume the investor still desires to make 4% per year. But this time the $1,000 annual cash flow stream grows by 2% each year. The investor would now be willing to pay $50,000 for that same $1,000 perpetuity because of the annual 2% growth rate in the income stream [$1,000 divided by (0.04 minus 0.02)]. In this case, a 2% growth rate doubles the price an investor would be willing to pay for the perpetuity, even though the year one income is identical.

A Key Reason Real Estate Appreciates

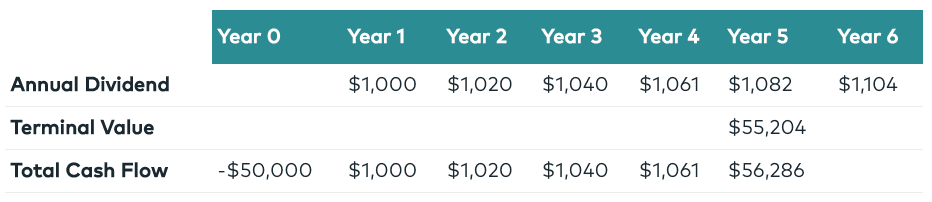

Most real estate investors don’t hold properties forever and look to achieve their return from both cash flow and value appreciation. One of the main reasons real estate appreciates is because the income stream is larger at the end of the hold period than when the buyer acquired the property. The example below illustrates what it would look like to hold the perpetuity, or a property, with a growing income stream for five years:

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | |

|---|---|---|---|---|---|---|---|

| Annual Dividend | $1,000 | $1,020 | $1,040 | $1,061 | $1,082 | $1,104 | |

| Terminal Value | $55,204 | ||||||

| Total Cash Flow | -$50,000 | $1,000 | $1,020 | $1,040 | $1,061 | $56,286 |

In this case, the investor paid $50,000 and held the investment until year five. The value of the perpetuity at sale, $55,204, is calculated by taking the year six cash flow and dividing it by the 4% expected rate of return, minus the 2% future growth rate of NOI [$1,104 divided by (0.04 minus 0.02)].

Expected Returns and Growth Rate

As you can see, a cap rate is a combination of both an investor’s expected return and the expected growth rate of NOI. That explains why a property with an 11% cap rate and an income stream expected to decline by 3% each year will generate the same returns as a property with a 5% cap rate and an income stream expected to grow at 3% per year.

11% Cap Rate: $25,000 / (0.08+0.03) = $227,272

5% Cap Rate: $25,000 / (0.08-0.03) = $500,000

In this example, both investors enter into the investment expecting to achieve an annualized return of 8%. But they get there in very different ways. Investors buying the property valued at an 11% cap rate would receive their entire return through cash flow and would lose principal value. However, the investor buying the property at a 5% cap rate would achieve their return through both cash flow and appreciation.

How Market Cycles Affect Cap Rates

Much of the real estate market’s cyclicality is a result of changes in expected returns, NOI growth expectations and actual NOI. In a market where property values are increasing, NOI growth is robust and past growth tends to lead to optimistic views of growth going forward. A large numerator (NOI) and a small denominator (cap rates) in the value equation combine to create expensive property values.

As the economy slows down, NOI declines and buyers dial back their growth assumptions, resulting in a smaller numerator and larger denominator in the valuation formula. The years following the 2008 recession witnessed cap rate expansion due to both credit risk, driving expected returns higher, and a dim outlook for NOI growth. Rising cap rates and depressed NOI created a situation of unprecedented value destruction. But it also created one of the greatest buying opportunities in the past 20 years. Over the ensuing decade, actual growth exceeded expected growth by a large margin and credit risk diminished.

Other Variables That Affect Cap Rates

Variables such as lease duration, discounts to replacement cost, geography and credit can impact cap rates. Longer lease durations generally command lower cap rates because uninterrupted cash flows tend to behave more like a long-term bond. Tenants with higher credit quality will drive rates lower, as will properties with high barriers to entry selling at or below replacement cost. In both of those cases, the income stream is likely to grow during the hold period. Conversely, properties with above-market rents valued far in excess of replacement cost are likely to command higher cap rates, as the cash flow would be difficult to replicate when the lease expires.

Additionally, cap rates work well for stabilized buildings with long duration leases, but the methodology breaks down when income streams encounter variability. A building that is 50% occupied with no income may have far more return potential than a building for sale at a 15% cap rate with a large, expiring tenant. Finally, a property with below-market rents would likely trade at a cap rate lower than the market rate. That’s because that income will increase substantially upon the expiration of the leases. The opposite is true of properties with above-market rents as those leases roll down to market levels.

Mitigating Cap Rate Risk

There is no way to know for certain where cap rates are going. But the risk to any real estate investment is that they are higher when you sell than when you buy. We counter this risk in two ways. First, we add value to every property we acquire with the intention of growing NOI by more than 25% during our hold period. Second, we drift cap rates higher throughout our hold period when we underwrite a new deal.

Increasing cap rates throughout the hold period is considered a best practice in underwriting. And it’s how we build in downside protection. For example, if market cap rates for stabilized properties are 5% today, then we use a cap rate from 5.5% to 6%, depending on our hold period, to determine our terminal value. Beware of any real estate investments that calculate terminal value using cap rates at or below today’s rates.

Cap rates cannot be used in isolation to value a property or to understand an investment’s potential. The cap rate is one of many tools we use at Origin when evaluating a property’s potential. Successful investing starts with buying right, and knowing how to value a property accurately is essential. As an investor, understanding how a cap rate works, when to use it, and its limitations can save time and money.

{kind=link}