A Message From Origin’s Co-CEOs Michael Episcope and David Scherer

During this volatile economic period, it can be a challenge for investors to keep up with, much less interpret, rapidly emerging economic data and trends. Distilling all this information so that you can make smart investment decisions that protect your wealth can sometimes seem almost impossible.

You’ve just opened our newest way to support our partners during this time: The Market Monitor. This newsletter will give you authoritative insights on how the economy and other trends are affecting the private multifamily real estate market, with critical perspectives provided by our “boots on the ground” investment officers. Our experts study this data every day and actively apply it to formulate and validate our ongoing investment strategy.

Every two weeks, our team leaders will report on how macroeconomic trends influence the private real estate market and shape our investment strategy down to our Funds and individual assets. Their goal is to empower our partners to become smarter, savvier and more confident investors, especially during periods of great uncertainty.

As investment managers in the multifamily real estate space, we have experience in navigating dramatic market cycles. Today, we’re using that expertise to scrutinize the big picture and the smallest details to find the best investment opportunities. Our priority continues to be protecting and growing the wealth of our investors. Now, more than ever, we believe that our investment partners will value the extensive risk-mitigation efforts that have positioned us as a top-decile investment manager. We are privileged to partner with you as we navigate the challenges and seek out new opportunities.

As Lending Tightens, Valuations Blur

Dave Welk, Managing Director of Acquisitions

The fog of uncertainty remains in the broader equity capital markets. With the private market transactions that we have seen, values for institutional Class A assets—which we develop and lend to through preferred equity—appear to have declined roughly 7% from their peak in late 2021 to early 2022. Values for value-add, 1980s-era and older vintages appear to be more impacted, largely due to the lack of bridge financing primarily used to acquire and renovate these assets.

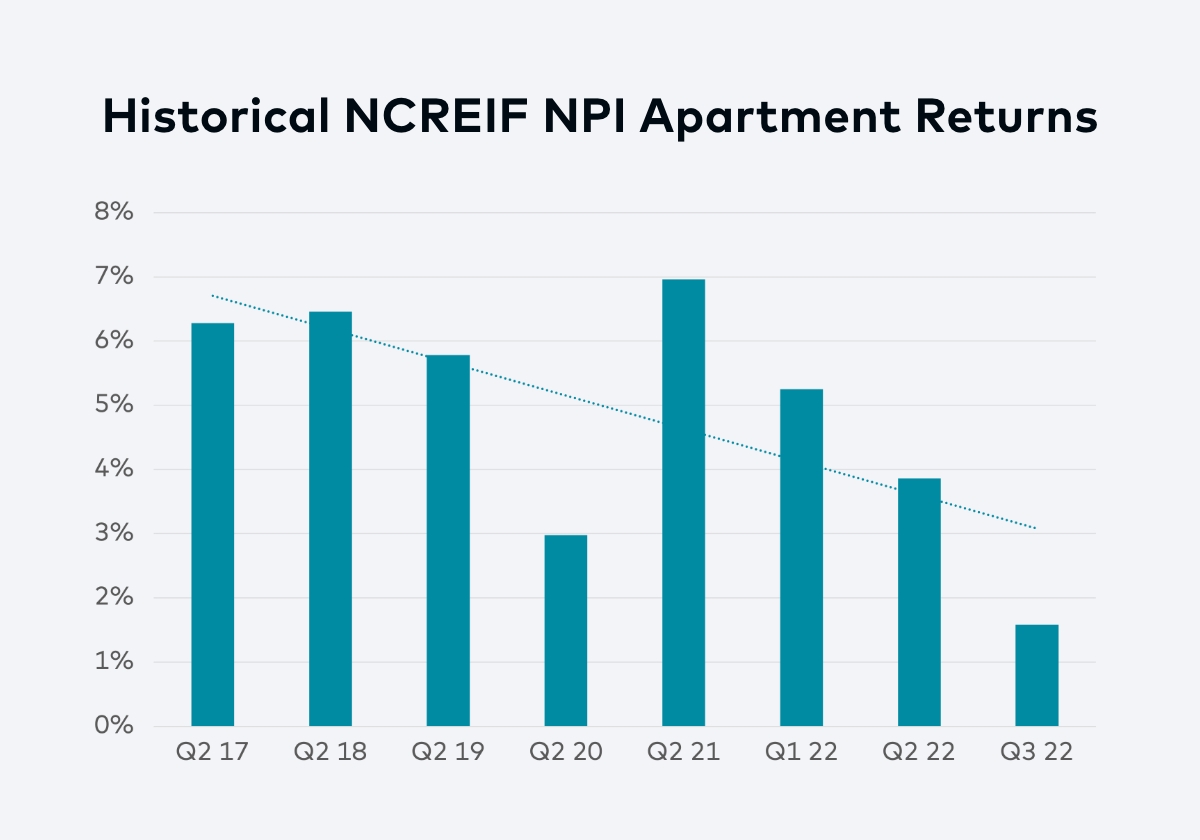

With the slowdown of the CRE-CLO market, debt funds are relegating financing of these assets to banks and insurance companies, many of which are maxing out at a more conservative 60% to 65% loan to cost. Cap rates are expanding and broadly settling in the 4% range across major markets, up from the 2021 low in the 3% range. All this suggests that values for value-add assets have fallen closer to 15%. This figure hasn’t shown up yet in the property index of NCREIF, which tracks the performance of U.S. commercial properties including apartments: Q3 2022 returns are 1.58%, a considerable deceleration from the 8.88% posted in Q4 2021.

Source: NCREIF

On the financing front, over the past 45 days, we’ve seen many regional and super-regional bank lenders stop quoting new construction projects for the balance of the year. Lenders remaining in the market are taking a much more conservative approach to underwriting, reducing leverage levels to 50% to 60% of cost. We believe the dislocation in the debt markets will provide opportunities for our preferred equity program over the next 12 to 18 months at even more protected positions within the capital stack at higher yields.

We have seen these cycles of lenders pulling back before. In 2015-16, new fiscal policy required additional capital reserves from banks that issued construction loans—a challenge for developers trying to secure construction financing. A similar situation emerged from May 2020 through early 2021 amid the pandemic. And we expect it to persist over the next year to 18 months as the Fed battles inflation by raising short-term borrowing rates.

Longer term, we see significant tailwinds for multifamily investment and development. The U.S. still has a shortfall of nearly 4 million multifamily and single-family units. The interim slowdown in development will exacerbate this problem. So, while we expect to see increased vacancies and concessions as we head into peak supply in mid-2023, we anticipate strong long-term demand.

Tightening Liquidity Breeds Uncertainty

Tom Briney, Managing Director of Acquisitions

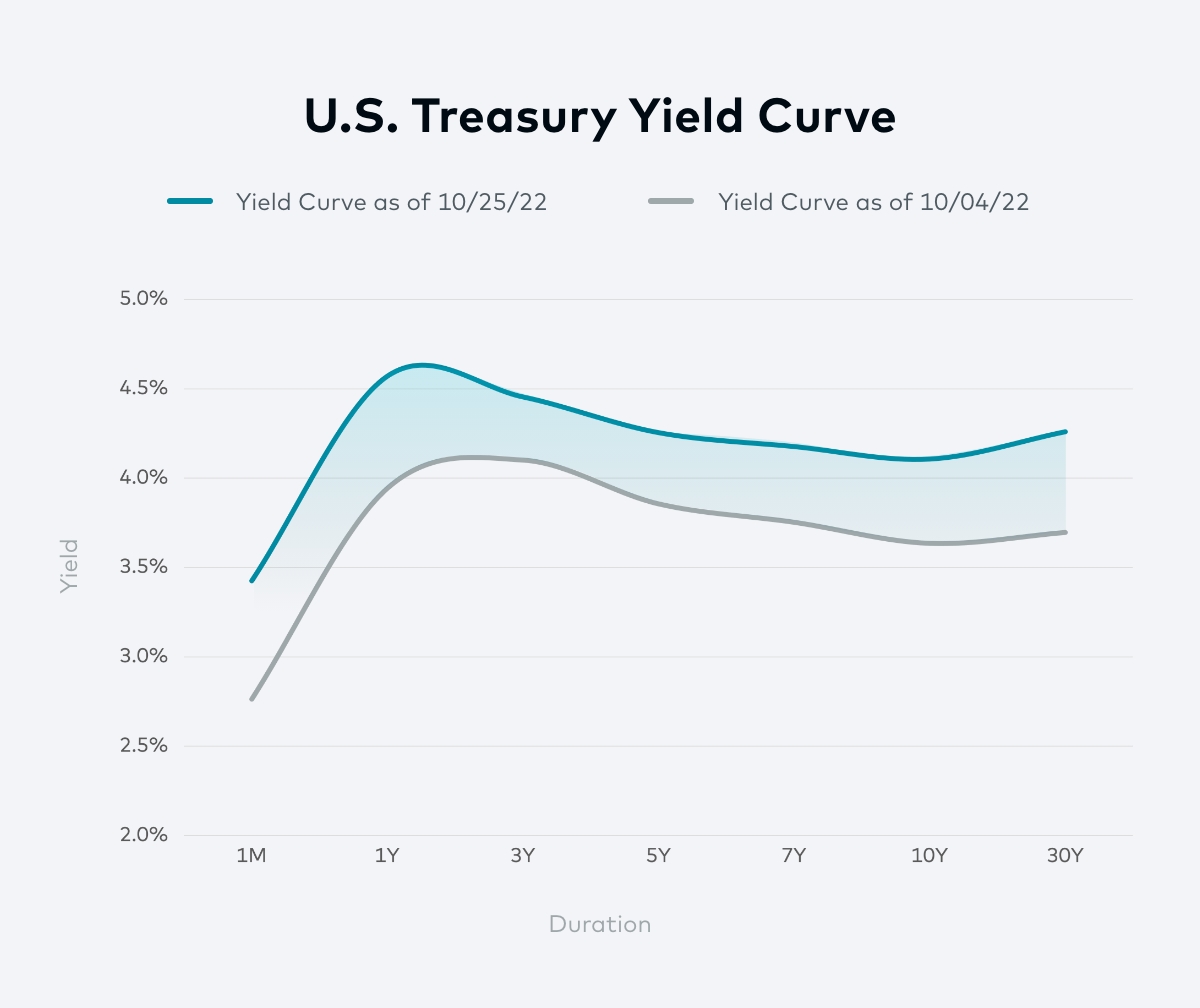

Both JPMorgan Chase and U.S. Treasury Secretary Janet Yellen have expressed worry about anemic trading volumes in U.S. Treasuries, which have not been this thin since April 2020. As trading volume, or liquidity, decreases, pricing volatility increases. For investors in the credit space, that volatility makes it difficult to know the relative value of current investments and whether it makes sense to buy or sell. Ultimately, this uncertainty incentivizes investors to take no action, which further exacerbates volatility.

As well, over the past two weeks, yields on shorter-term and longer-term Treasury bonds have risen, pointing up the inverted yield curve that historically has signaled an impending recession (see chart below). But the U.S. Treasury is not alone in this world of tightening liquidity.

Source: Bloomberg

The commercial real estate space has been experiencing similar challenges since the summer, with price discovery continuing with every new commercial real estate collateralized loan obligation—CRE CLO—or trade on the secondary market. Yields on the BBB and non-rated tranches have been so attractive that issuers are electing to hold them on their balance sheets, further limiting trading volume and liquidity.

Tightening liquidity and widening spreads in the public credit markets directly impact cash flow and values of private real estate investments. Many of the largest originators of real estate loans utilize the public credit markets to sell loans to investors; they do that to free up their balance sheets so more loans can be originated. As volatility persists in the public markets, originators increase the interest rates they charge to borrowers—or even stop lending entirely.

Price discovery also is happening in Freddie Mac’s B-Piece market, which has been exceptionally quiet as many buyers elect to move to the CRE CLO market in search of better relative value for their purchases. It’s difficult to make transactions right now—in general and within Origin’s Multifamily Credit Fund, which comprises B-Pieces—because of the bid-ask spread and the limited options in bonds. We’re scouring potential sellers in the B-Piece space and looking for relative value and reduce the bid-offer spread. Expect trading volume in this space to continue to be low, until inflation subsides enough to produce some clarity in pricing, or until a market shock forces levered buyers to sell at steep discounts.