Tom Briney, President and Chief Investment Officer, Origin Credit Advisers

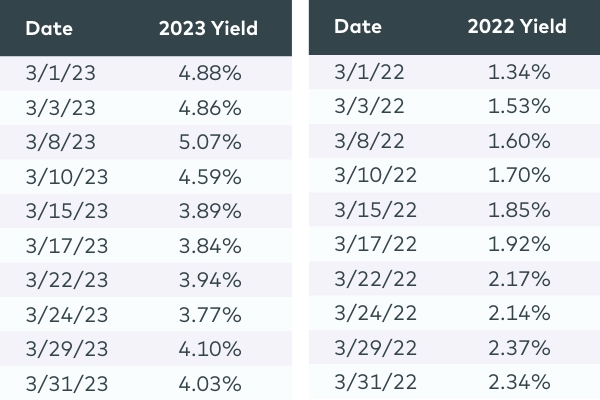

March 2023 may go down as one of the busiest months for economic developments and market volatility since the start of the Global Financial Crisis in 2008. The market has been digesting the collapse of three banks, the merging of two “too big to fail” banks, and a further interest rate increase by the Federal Reserve. Add to that the drumbeat of tech-firm layoffs and OPEC’s more recent announcement that it would cut oil production, and you have some spectacular market swings exactly one year after the economy began responding to the first of nine (so far) interest rate hikes. The chart below reflects that economic volatility.

Two-Year Treasury Bill Yield Comparison, 2022-23

Source: Bloomberg

All that news was almost exclusively negative. But investors in the equity market and investors in the debt market are reacting in two very different ways. The S&P 500, widely accepted as a barometer of the health of U.S. corporations, finished March at a nearly 3.6% increase from the previous month. Conversely, over those same 31 days, investors flocked to the safety of U.S. Treasury Bills, pushing the yield on the two-year bill down by 88 basis points to 4.03%, or 17%.

Both equity and debt investors appear to be operating within the economic volatility with some certainty, albeit in different directions. Equity investors seem to be reflecting renewed confidence in the health of the economy, and debt investors appear to be harboring near-term fears and a strong desire to protect their capital.

One approach isn’t necessarily better than the other. A lot is happening day to day—economic news, endless iterations of market changes, all seemingly contradictory data that isn’t pointing in a single direction. An investor’s choices, though, are more straightforward: Dive into the market—any market—or park their money somewhere risk-free and ride the situation out, no matter how long it takes.

As an investment manager, risk is part of just about every decision I make. My view is this: In environments where more risk is present, you don’t stop investing. You just move into a more protected position. In some cases, that might mean lowering the amount of leverage in a particular deal. In others, it might involve being the grownup in the room when a deal is being discussed. Sometimes that moderating voice comes from the bank; in our business, it’s generally the limited partner or the preferred equity provider. And even with all the economic data flying around, I’m observing “risk-on” attitudes from dealmakers focused more on the potential payoffs than the existing threats.

Does this explain the perceived disconnect among different types of investors? Maybe. If you operate in the investing space, you know the credit market has historically tended to predict economic ups and downs more than the equity markets. The inverted yield curve is curving right down into a possible recession, but the S&P seems to be channeling a sunnier outlook.

An investor looking for guidance in this market volatility will struggle to interpret what is happening right now, but it helps to look more like three to 12 months into the future. I don’t know who’s right and who’s wrong, but I do know the Fed’s rate increases are having their desired effect of slowing inflation while also trimming parts of the economy which had become bloated, along with some other effects.

There are still opportunities for investors, but it’s necessary to look harder and expand the menu of options to find them. Even with a potential storm coming, there are ways to invest capital that are defensive in nature, and I’m looking in the credit markets for those opportunities. I also know that the last layoff, business failure and lost fortune haven’t yet occurred. Until they have, we can expect continued market volatility and uncertainty. Don’t get indigestion by overanalyzing the day-to-day market fluctuations.

What Are Developers Waiting For?

Ken Lodge, Associate Vice President of Investment Management

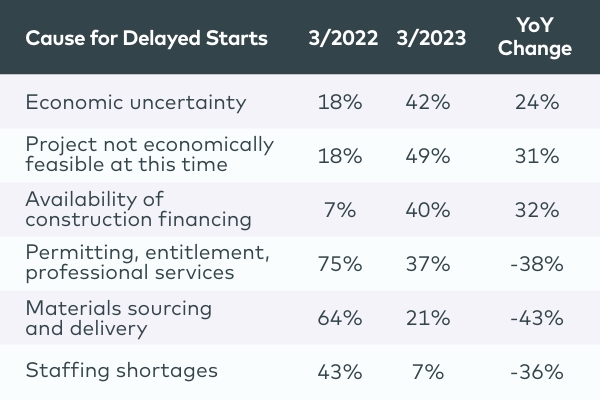

On March 27, the National Multifamily Housing Council (NMHC) released its Quarterly Survey of Apartment Construction and Development Activity. According to the survey, 88% of respondents are experiencing delays, a modest increase from 85% in the March 2022 survey. However, when asked which factors caused the delays, responses were starkly different than the previous year.

Cause for Delayed Construction Starts

Source: National Multifamily Housing Council

These results reflect one obvious outcome of the Federal Reserve’s actions on interest rates: unfavorable conditions in the debt capital markets. According to the Federal Reserve Economic Data (FRED), new, privately owned housing unit starts through the first two months of 2023 fell 19.5% year over year. That’s not necessarily bad news: The runaway escalation in construction costs in 2021 and the first half of 2022 has cooled significantly. When asked whether they had seen deals repriced over the past three months, 47% of developers said they had seen deals repriced upward, versus 92% in March 2022; 21% said downward, versus 0 in March 2022; and 14% said they had not seen repricing, versus 5% in March 2022. Still, with the tightening credit environment and a pessimistic near-term outlook for rents in mind, developers have begun questioning—with good reason—whether the juice is worth the squeeze.

According to the survey, the leading cause of delayed construction starts is that projects aren’t “economically feasible at this time”—reflecting that developers are playing the waiting game and hope that conditions improve soon. What must change for projects to become viable again? There are innumerable variables, but for now let’s consider the following:

Land values: Though limited transaction volume over the past nine months has made price discovery a guessing game, there remains a clear disconnect between what sellers are willing to accept and what buyers are willing to offer. The first sellers likely will be owners that purchased with debt and are forced to sell at a discount. Still, even owners that purchased with cash have to consider whether they can stomach carrying costs until market volatility calms down and opportunities become more compelling.

Construction costs: As Origin Senior Vice President of Development Kevin Miller pointed out in a recent Market Monitor, material prices have come off their early 2022 peak—a conclusion supported by the NMHC survey. But a steep reduction in building costs is unlikely; based on historical results, we should expect to see prices face downward pressure in 2023 and potentially 2024 before returning to stable growth. That said, a return to pre-COVID pricing seems exceedingly unlikely.

Financing costs and availability: These may be the biggest question marks regarding near-term prospects for development activity. How does the Fed balance its priority of taming inflation with concerns that continued rate hikes could result in a hard economic landing? Uncertainty regarding rate hikes could be exacerbated by the recent turmoil among regional banks, which will likely result in a more onerous regulatory environment and further tightening of credit availability, as Origin Managing Director of Acquisitions Dave Welk recently discussed.

Revenue potential: According to our own research, rent growth has slowed and even gone backward in many major markets. We expect this to continue through 2023, as nearly a million new rental units may be delivered, according to the U.S. Census Bureau—more than at any time since the 1970s. Supply shock will result in near-term elevated vacancy rates and downward pressure on rents, stifling investors’ returns for taking on development risks. But a continued supply/demand imbalance means these new units will eventually be absorbed and, coupled with a dip in medium-term deliveries due to the current slowdown in starts, rent growth will recover in 2024 and beyond.

It’s clear that we are at the beginning of a slowdown after a period of record-setting development activity. In the near term, we expect to see elevated vacancy levels and downward movement in effective rents as operators compete with discounts and concessions to fill their newly built assets and return markets to stabilized occupancy rates. Should a sharp recession materialize—we are predicting such an event by October—it’s likely that the Fed will return to a more favorable rate environment to spur the economy. That could support the construction of new apartments—for which demand far outweighs supply, even after the construction boom of this past cycle. While we see a bumpy short-term forecast, it may be just what’s needed to stabilize fundamentals over the longer term and preserve the risk-adjusted returns that underpin our multifamily investment strategy.