This is our final Market Monitor for 2022. We’ll be taking a short break and resuming publication on Jan. 14, 2023. From all of us at Origin Investments, we wish you a joyous holiday season and a prosperous New Year.

Risks and Opportunities in 2023

Dave Welk, Managing Director of Acquisitions

Commercial real estate has been less susceptible to wild market fluctuations over short periods. But over the course of this year, our industry has experienced unprecedented volatility, looking more like the hedge fund space than ever. Our benchmark index rate, the U.S. 10-year Treasury, experienced one of the most volatile periods on record. This rate is widely used as the base index for pricing both long-term financing rates and, when a risk spread is applied, in determining stabilized cap rates. In January, it was around 1.60%. It nearly doubled to 3.13% in early May and peaked in mid-June at around 3.50%. That included some wild daily swings of 20 basis points or more (that’s 6% to 8%).

After retreating to the mid-2% range in July, yields spiked in late October at nearly 4.25%, an eye-popping 266% increase from January. This volatility, for an industry with limited liquidity due to the time it takes transactions to close (often 90 days or more), created some significant challenges: for buyers to accurately price dynamic changes in interest rates, for lenders to hold interest rates, and for sellers to fully grasp these impacts on pricing and asset value.

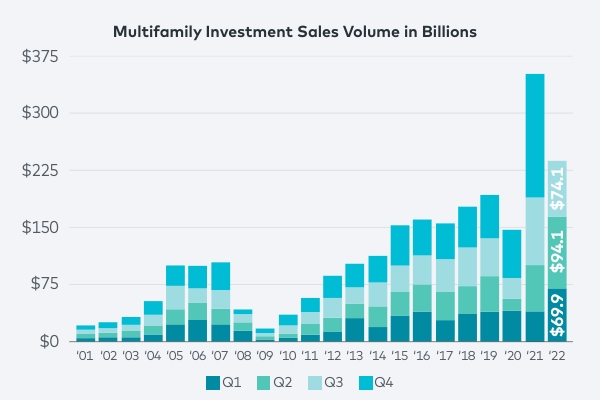

As a result, sales activity for multifamily assets have declined steeply since June. Through 3Q 2022—although transaction volume to date was at a 20-year high of $238 billion—quarter-over-quarter transaction activity declined 21% from 2Q 2022. We expect the decline to continue when Q4 numbers are posted, and to represent a sharp decline year over year compared with 4Q 2021’s record volume of $163 billion.

Sources: Newmark Research, MSCI Real Capital Analytics

As we head into 2023, what does this mean for the multifamily market?

Opportunities: Developers and owners will continue to need preferred equity and mezzanine debt to fill the hole in the capital stack left by the continued retrenchment by lenders. Assets with loan maturities coming due in 2023 likely will face a shortfall of refinance proceeds, and fresh capital will be needed to pay off balances. There will be some forced selling—due to lack of capital, fund life issues, estate planning or, in some cases, long-term owners with a sizeable gain to capture who still desire to sell. We believe that quality acquisition opportunities may emerge later in 2023, with the largest opportunities in older vintage, Class B and C assets financed with short-term bridge financing that face loan maturities in 2023. We also expect to see a few opportunities to acquire higher-quality assets as some institutional investors remain on the sidelines.

We anticipate that the Fed will continue to execute its strategies to curb inflation. If the Fed’s communication and actions are consistent, some stability will be provided to the capital markets. The desire by the Fed to unequivocally stamp out inflation will likely push the U.S. economy into a recession, which we believe will occur in late 2023, precipitating interest rate declines shortly thereafter and into 2024. Declining interest rates may help stabilize further price declines and lead to an uptick in values.

Given the overall slowdown in construction activity, we anticipate construction costs to level and decline over the year, potentially as much as 5% or more from the 2022 peak. In markets like Tampa and Phoenix, where land prices increased sharply over the past two years, we expect some decline in the market value for land. As a long-term investor, we believe our Sunbelt and Mountain target markets have durable fundamentals, and we expect to continue to find quality development opportunities over the next year and beyond.

Risks: Debt maturities are the biggest risk in 2023, but they also will provide some of the best opportunities for investors. Declining investor sentiment, exacerbated by rent declines—which we forecast will continue into 2023—and recessionary pressure, is another risk. This risk could ultimately be tempered by a decrease in interest rates. Further declines in the stock and bond markets could complicate portfolio allocations for institutional investors, who strive to maintain a fixed exposure to commercial real estate. This could remove significant liquidity from the market, causing property values to fall further. Last, a record 565,000 multifamily units will be delivered across the U.S. in 2023, putting downward pressure on rents and requiring developers and owners to increase concessions to lure renters.

Disciplined investors with access to debt and equity capital are likely to find quality, long-term investments in 2023. Next year may represent the first of several years of opportunities for investors.

Keeping an Eye on the Fed

Tom Briney, Managing Director of Acquisitions

As we wind down an adventurous 2022, it’s always fun to think about what was done well, what was done poorly and where we are grateful to have had luck on our side. While I can point to numerous examples for all three categories, looking forward to the new year is probably a more productive exercise. The three items I will be watching closely in 2023 are the Federal Reserve’s funds rate, the Fed’s balance sheet, and the capital markets’ reaction to both.

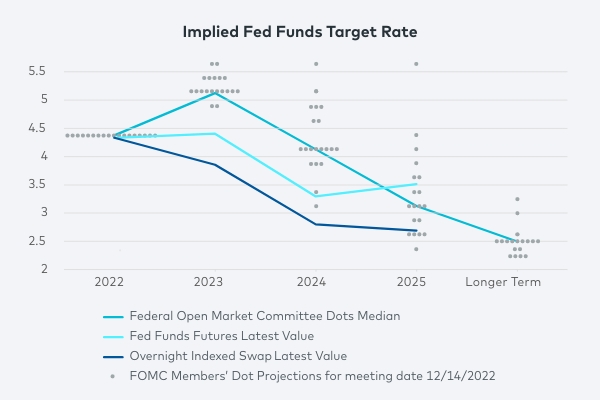

This past year, the Fed made some extraordinary moves, increasing its overnight lending rate, the Fed funds rate, from 0% to 4.5% in a matter of months. Market participants generally expect another 50 to 75 basis points of increases in the first quarter of 2023. This is consistent with the Fed’s “dot plot” (see chart below), but the expectations of market participants and the Fed begin to deviate in the second half of the year.

Fed Chairman Jerome Powell has been opaque in setting expectations on the Fed Funds rate, only indicating that most market participants are overly optimistic in their rate cut expectations. Even with recent positive news on inflation, I will take Powell at face value and consider a cut in 2023 off the table. However, folks would be wise to listen for any deviation to his messaging for more clarity as to when a cut may come.

Source: Bloomberg

An often-overlooked arrow in the Federal Reserve’s inflation-fighting quiver is the reduction of its balance sheet—a direct reduction of money in the economic system, or M2. Throughout 2020 and 2021, the Fed pumped trillions of dollars into the economy by buying agency-backed bonds, and even corporate-backed bonds, in a process known as quantitative easing. During a period of neutral monetary policy, the Fed will neither add to, nor reduce, its balance sheet holdings, keeping its contribution to M2 static.

Now that the pace of the world economy is driving inflation well above the target of 2%, the Fed is focused on quantitative tightening, or reducing its balance sheet. It does this by either allowing bonds to be paid off at expiration, rather than roll them over into a new term, or actively selling bonds with longer maturity dates. In either case, money is being given to the Federal Reserve, not reinvested into the economy—effectively reducing M2.

Controlling the Fed funds rate and the balance sheet affect inflation and economic growth. However, moves in the Fed funds rate can have a more dramatic impact on the economy as a whole relative to balance sheet reduction. Look to the Federal Reserve to use its balance sheet size to fine-tune monetary policy long after rate increases cease.

If we’ve learned anything in the second half of 2022, it’s that market participants will maintain irrational optimism until irrational pessimism takes over—with the transition taking very little time. With nearly 80% of the U.S. GDP driven by consumer spending, extended periods of negative sentiment can be a self-fulfilling and self-perpetuating drag on the economy. Market observers will get a hint in early 2023 if the negative cycle can be broken before the Fed begins easing again, or if the negative wealth effect will take hold and extend any potential economic softness.