Will Renewed Capital Markets Optimism Last?

Dave Welk, Managing Director of Acquisitions

Last week, members of Origin’s investment teams descended upon Las Vegas to attend the multifamily industry’s premier annual conference. After three days of meetings and conversations with capital markets participants, including national and regional developers, investment sales and structured finance brokers, lenders and operators, a theme emerged: a renewed sense of optimism among the broader capital markets for 2023. This came as a bit of surprise to us, given continued challenges in the financing markets and that some of the operational challenges we have been forecasting are being realized.

That said, as highlighted previously, an estimated $350 billion of capital raised by private equity investment vehicles is targeting U.S. commercial real estate for deployment this year. Based on our conversations, it was clear that this dry powder wants to find its way into the market, buoying the optimistic sentiments. Here are some overarching takeaways from our meetings:

Transaction activity will pick up in the near term: An initial wave of asset sales will come to the market over the next several weeks after a slowdown in transaction volume in 3Q and 4Q 2022. This is important as many eager investors are waiting to observe transaction data—including pricing and corresponding tax- and insurance-adjusted cap rates—before wading back into the marketplace. Once these transactions close in the next quarter or so, the market will have some visibility on valuations in an operating and lending environment that is decidedly different than the mid-2022 peak. Expectations are that the market will experience a significant uptick in transaction activity in the back half of 2023.

Some lenders are returning to the market, and terms are improving: As construction lenders retreated from the market and permanent lenders tightened underwriting standards in 3Q and 4Q 2022, debt proceeds were reduced, and all-in interest rates increased. While some money center banks remain largely out of the market, insurance companies have ramped up construction lending to fill some of this void. Further, for the first time in more than two quarters, Fannie Mae and Freddie Mac are providing some much-desired permanent financing options that are available at sub-5% rates. The upshot of this is that concerns about negative leverage (borrowing at interest rates that exceed a property’s cap rate) may be somewhat abated and prevent cap rates from expanding to 5% and beyond.

Construction and land costs may see adjustments: Development equity capital has increased target returns, which will result in many construction projects either being put on hold or scuttled altogether. The reduction in activity is likely to lead to future relief in subcontractor pricing. The bid-ask spread between landowners and developers seeking to capitalize projects under this new paradigm remains wide, and it’s likely that land prices adjust in coming months.

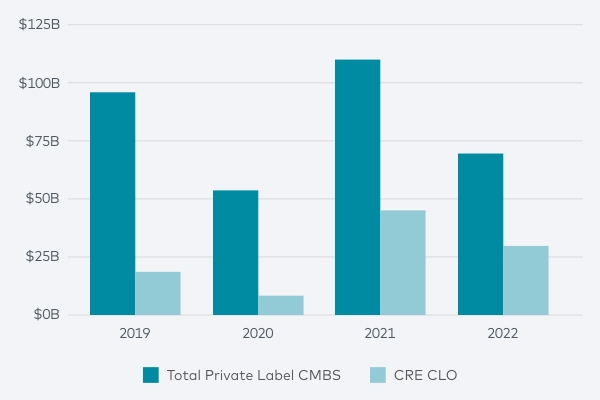

Most ‘distressing’ conference statistic: The most likely market segment to experience near- to medium-term distress are the buyers that purchased older properties at heightened valuations over the past 12 to 24 months using high-leverage, short-term financing, also known as bridge financing. To provide some context of the size of this potential opportunity set, the majority of bridge financing was provided by the commercial real estate collateralized loan obligation (CRE CLO) segment of the market, which, as shown in the chart below, comprises $84 billion of originations from 2020 to 2022. Most of this debt was originated on a 24- to 36-month term, indicating that initial maturities will commence this year and increase in to 2024.

CMBS and CRE CLO Origination Volumes

Source: Green Street, Commercial Mortgage Alert

One mortgage broker framed this challenge well: If a property was purchased at a 3.25% cap and the owner used an 80% loan-to-cost bridge loan at acquisition, the owner would have to generate an 80% increase in net operating income to achieve a cash-neutral refinance (meaning they wouldn’t need additional capital to pay off the maturing loan) based on current underwriting standards of permanent lenders. Even if these owners were operating in our most robust markets of Phoenix and Tampa, which experienced 20%-plus rent growth over this period, there would still likely be a need for a rescue capital investment upon loan maturity.

As the year unfolds and if our projections for continued rent and occupancy declines take hold, it will be interesting to see if the current optimism in the capital markets remains. No matter what, one larger theme remains: Over the long term, multifamily investment represents one of the best segments within U.S. commercial real estate for capital allocation.

The Slow Thaw

Tom Briney, Managing Director of Acquisitions

The last 30 days of 2022 were marked with uncertainty and inactivity, neither of which is good for markets. The uncertainty around the rate of inflation and the pace of Federal Reserve interest rate increases had a profound impact on sentiment, which ultimately led to investors sitting on the sidelines until more clarity was available. That put a chill on the markets—but as it turns out, changing the calendar from 2022 to 2023 was all that was needed to trigger a thaw.

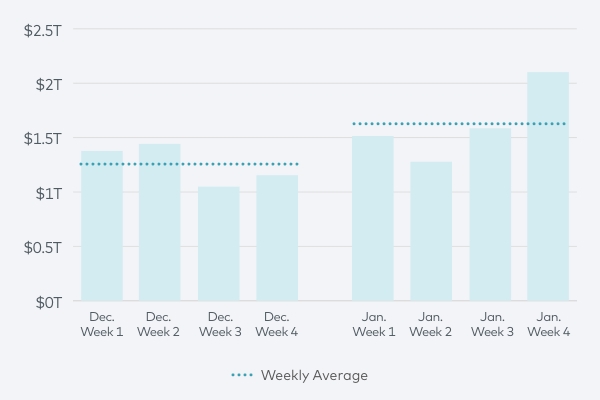

The month of December 2022 averaged roughly $1.3 trillion in U.S. Treasury trading volume each week, meaning that roughly that amount of U.S.-backed bonds and bills traded hands every week. By the end of January, that had increased 30% month over month to more than $1.6 trillion in weekly volume, with momentum picking up greatly to hit $2.1 trillion in the final week. This relative thaw in the Treasury market is resulting in lower interest rates on the middle and long end of the yield curve (three-plus years), with yields compressing 30 to 40 basis points. As we’ve mentioned previously in Market Monitor, the Treasury markets directly impact all other credit markets—including the market for multifamily loans.

Average Trading Volume, U.S. Treasury

Source: Financial Industry Regulatory Authority

As Treasury liquidity continues to improve, that rate compression is percolating down to all corners of the debt market. Financing from Freddie Mac and Fannie Mae, life insurance companies and even bridge lenders is becoming more available, and potentially more affordable. This, in turn, will result in more transaction activity—buying and selling of physical buildings—helping to establish clear values of investment portfolios across all asset sectors, which have seen anemic trading volume since Q3 2022. With transaction activity accelerating, investors will gain substantial clarity on the value of their investments and will have the information they need to buy and sell as they have done in the past. That results in more transaction activity, and the cycle builds again.

The U.S. Treasury market is the leading indicator for all other credit markets in the United States and, arguably, the world. While we are not completely in the clear yet, the fourth-quarter chill that blew into that corner of the market seems to be thawing out. Brighter days are ahead—or at least more activity in the credit and private equity space.