Origin’s Qualified Opportunity Zone (QOZ) Fund II pairs high-potential development projects with capital gains investments that combine to create benefits for communities and investors alike. The projects in this multifamily investment Fund are in the path of growth—that is, in already transforming neighborhoods that show likelihood of returns even before the additional tax benefits of a QOZ.

Last year saw some dramatic economic shifts: Accelerating inflation, which peaked in mid-year, along with aggressive interest rate increases. Multifamily rents increased earlier in the year while the housing market began to cool. While we are starting 2023 with the expectation that Federal Reserve moves to curb inflation, among other factors, are likely to trigger a recession, we view the long-term outlook for multifamily investment as positive. And we continue to position this Fund for long-term, tax-protected returns. However, it’s critical for us as risk managers to test our assumptions under a variety of economic scenarios, which these stress tests will provide.

The QOZ Fund II is our second Fund that benefits from the Qualified Opportunity Zone (QOZ) program, which was created under the Tax Cuts and Jobs Act of 2017 to encourage real estate investment in targeted zones across the U.S. Investors using capital gains to invest in QOZs can receive significant tax advantages. Bipartisan legislation introduced in April 2022 would have extended the availability of some tax benefits and increased reporting requirements for fund managers, but the year ended before the bill was acted upon. It’s uncertain whether another version will be introduced in the new session of Congress.

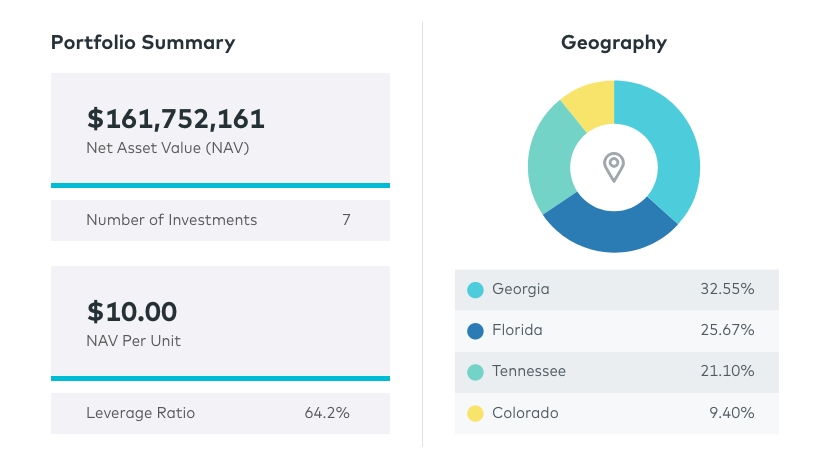

QOZ II Summary and Current Portfolio

The Fund’s portfolio consists of Class A, ground-up development projects in Georgia, Tennessee, Colorado and Florida. Once built, the properties will be held in a diversified portfolio that produces stable cash flow. In order to meet the program’s 10-year hold requirement, QOZ properties must be owned and operated for at least five to seven years after construction. QOZ Fund II has a cap of $300 million and a close date of Dec. 31, 2023. So far, $231 million has been raised. The Fund is currently targeting investment in at least seven development projects capitalized with an estimated $283 million in total equity. As of this writing, we are navigating pre-development activities on six of the projects, and construction is underway on the seventh, Elan Rio Grande. Project values as of Sept. 30, 2022, are held at the cost of acquiring the land sites. The exception is Elan Rio Grande, which reflects a small markup in value based on construction progress.

How We Value Developments in the Fund

The value of a development project is primarily a function of the future cash flow and residual value of a completed and fully leased property. As a project progresses through development—and as uncertainty around the timing of completion and other costs are removed—the investment risk is mitigated. As a measure of risk, the discount rate, or internal rate of return, applied to future cash flow is highest at the beginning of construction but compresses over time. For more details about how we value the Fund, read our valuation policy here.

As we underwrite our current projects, we are actively monitoring development costs to ensure that our margins remain compelling. In today’s environment, that includes assessing rising interest rates, changing construction and labor costs, capitalization rates that have increased from less than 3.5% to around 4.5%, and the effects of inflation. It also includes cooling rent forecasts—some of which are moving into negative territory—in the areas where we invest (see the chart below).

The value of fully leased property relative to the cost to develop is the gross margin. We require a minimum gross margin of 30% for our development opportunities at the time of underwriting. That means that a couple of projects are being re-engineered to create a more affordable design that still has the same value for the renter. In other cases, as the environment shifts, we may decide that the risks are no longer worth the potential rewards.

How We Account for Changing Scenarios in 2023

The possibility of lower rents has been factored into our underwriting process for the past year, along with the increasing likelihood of a recession. Both scenarios have been predicted by Origin MultilyticsSM, our proprietary suite of machine-learning models. But the QOZ II Fund is a long-term investment, and we have chosen markets that we believe will rebound strongly to the five-year growth average. The chart below represents the markets in which QOZ II invests, and their weighted average five-year rent growth forecast, according to Multilytics.

Stress-Testing Properties in the QOZ II Fund

Part of our underwriting process includes stress-testing each investment in our portfolio to determine whether it can withstand falling rents, increasing development costs and higher cap rates. In the chart below, we compare the property’s original pro forma with the recession rent forecast (far right).

The investments in this portfolio were underwritten assuming an average 62% senior debt and an average return on cost of 6.0%. The return on cost is calculated by taking the net operating income at stabilization and dividing it by the cost of the project. The difference between the return on cost and prevailing cap rates represents the project’s gross margin. The column on the far right shows the returns using Multilytics’ recessionary rent-growth forecasts and a 5.0% cap rate. The “multiple at 5.0% cap rate” column captures the return on our investment using Multilytics’ forecast rents and a 5.0% cap rate. The next column, “% of rent decline to breakeven,” represents how much these predicted rents would have to decline before our capital is at risk.

Source: Multilytics

In several cases above, Multilytics’ rents are higher than our pro forma underwritten rents. That’s because when we underwrite a deal, we employ the concept of margin of safety—we present both the forecasted rents and the rents that make the deal work. Forecasted rents always are the ceiling. If the project can work with a lower rent, then that’s how it is approved. The underwritten rents above represent the approved rents.

The Fund is invested in Opportunity Zone sites that have high potential to grow, expand and are located near existing lifestyle amenities—shopping, entertainment and other activities that attract renters. While the Fund’s portfolio will exist for 10 years, we won’t have to wait that long to see these areas reach fruition. We can see the improvements and potential today. We are protected by our development margins and our discipline around risk management. All of that adds up to the creation of long-term value—and significant tax benefits—for investors.