Qualified Opportunity Zones were designed to spur economic development by offering investors tax incentives to invest in real estate or businesses in distressed areas. Yet QOZ investments vary widely, so unlocking these potentially substantial tax incentives depends on the caliber of the asset and its performance over time. Several rewarding tax benefits, however, give these growth-oriented assets the potential to provide greater total returns than similar non-QOZ investment strategies. These benefits range from tax deferral to tax-free appreciation.

Many early investors in the Qualified Opportunity Zone (QOZ) program received a 10%-15% step-up in basis on capital gains taxes if a Qualified Opportunity Fund (QOF) investment is held for five to seven years prior to Dec. 31, 2026. That benefit expired on Dec. 31, 2021, but other tax benefits offered by the program continue.

Here are six compelling reasons investors should consider adding QOZ investments to their portfolios:

1. The Ability to Defer Capital Gains Taxes

Investors who have realized short- or long-term capital gains from selling a business or other asset—be it equities, real estate, real property or alternatives like art or rare coins—can defer the taxes on those gains through the end of 2026 if they invest them in a Qualified Opportunity Zone Fund. However, capital must be invested no more than 180 days (about six months) after they have closed on a sale. Capital can’t simply be pledged as a future commitment to, for instance, a private equity real estate fund that issues capital calls when it is ready to close a deal. So, taking advantage of this 180-day deadline requires investors to identify fund managers who can generate a predictable flow of QOZ deals—a tricky proposition since the timing of real estate closings can be fluid and often delayed.

There are some exceptions, however, to the 180-day rule. For direct personal investments like the sale of a stock or REIT, the 180-day period starts on the date the gain is recognized. Also, there are special rules for capital gains from partnerships, S corporations, beneficiaries of estates and non-grantor trusts. According to the Internal Revenue Service, the 180-day investment period for these gains is allowed to start on the last day of the entity’s taxable year; the same date that the entity’s 180-day period begins; or the due date for the entity’s tax return, without extensions, for the taxable year in which the entity’s realized the eligible gain.

If investors sell or exchange their QOF shares before 2026, they must settle taxes at that time. However, the capital gain’s original tax attribute is preserved throughout the deferral period. If investors had a short-term capital gain, the same short-term tax treatment applies when the deferred taxes are paid for that gain. The same applies for long-term capital gains. In any event, the taxpayer’s deferred capital gain is recognized in the 2026 tax year. So, a QOZ investment may defer taxes on the capital gain reinvested into the QOF—but not lower them.

2. Eliminating Capital Gains and Exiting Tax-Free

Investors who hold their QOF investments for a minimum of 10 years will reap the greatest reward offered by the QOZ program: the ability to exit the investment without paying any federal capital gains taxes on any appreciation realized from the investment the entire time it is held in the QOF. Many investment programs offer the opportunity for tax deferral. But QOZ investments offer the opportunity for tax elimination without any additional requirements other than meeting the 10-year holding period.

This tax benefit can be realized beyond Dec. 31, 2026, when the QOZ investment program is set to expire, according to current legislation. Taxpayers who invest up to that date can hold the investments and continue earning appreciation tax-free until June 2047, as long as a QOF remains operative. Many Opportunity Zones were originally undercapitalized, distressed areas that showed potential for sustained economic growth. So, the complete exclusion of post-investment appreciation from capital gains taxes could save a significant amount of money on a successful investment.

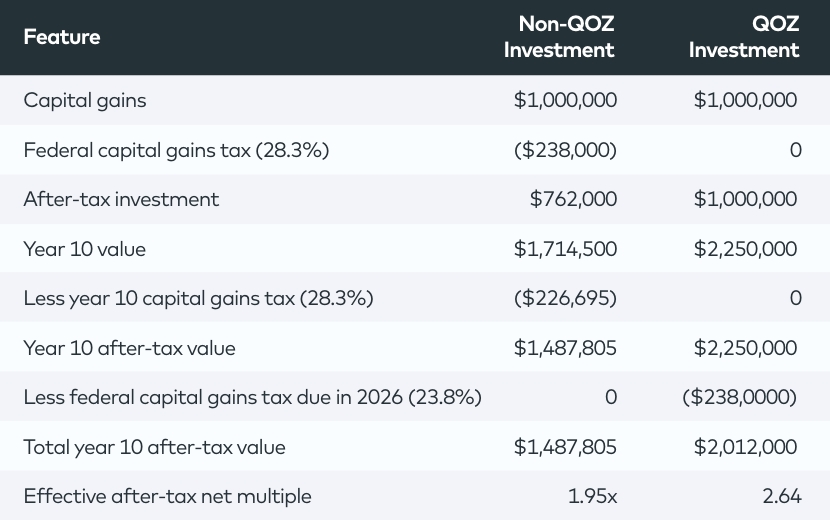

The benefit of having a QOZ property is that federal capital gains taxes are deferred until the investor exits the investment totally or if the property is held 10 years or longer (see chart).

3. The Ability to Shelter Income Distributions from Taxes

For real estate investments in a QOZ, once the asset is stabilized. That means it has been built or undergone planned renovations, achieved a certain occupancy rate (typically at least 90% of all units) and achieved a net operating income strong enough to support debt service—it will produce income. Income generated by real estate investments can be shielded through depreciation and deductions.

Depreciation, the tax-based decline in value of an asset over time, implies a loss. But the opposite is true when it comes to real estate investing. A property’s value often decreases—or depreciates—over time due to wear and tear of appliances, fixtures and finishes. This reduces the property’s net operating income, or NOI. So, tax law allows real estate owners to take a deduction for the property’s depreciation to alleviate current or eventual capital expenditures.

Let’s say a property’s pretax net income is $70,000 and the total depreciation expense is $30,000. The taxable net income is $40,000, allowing the rest of the taxable income to be sheltered.

4. The Ability to Eliminate Depreciation Recapture Tax

Depreciation applies to all investment properties. But for properties that are not in a QOZ, investors must pay depreciation recapture taxes on the depreciation deductions they took on a property during the time they owned it. The tax liability is generated when the asset is sold. A 25% tax rate is applied for the year of sale. That makes it one of the highest taxes associated with the sale of a depreciable real estate asset. It’s second only to real estate owned less than one year that is taxed as ordinary income and could be as high as 37% (depending on an investor’s tax rate).

But for QOZ properties, the 25% depreciation recapture tax is eliminated when the asset or QOF shares are sold after 10 years. That happens even though an investor benefited from depreciation while they held the property in a QOF. This is a key, but perhaps underappreciated, reason investors are able to boost their earnings on a QOZ investment.

5. The Potential to Earn Excess Depreciation

Nothing is static when managing an investment property. In some years NOI could be low, such as when a building is just starting to stabilize and has a lower occupancy rate, or if net operating expenses go up. In some years, depreciation may exceed distributions of operating income—the passive income from a QOZ investment.

When that happens, investors can use those excess passive losses, or excess depreciation, to shelter passive investment income they may have from unrelated investments. They may also carry this excess depreciation forward to be used in the future. The onus to use this potential benefit, however, is on the investor. A sponsor or manager would report this information on a K-1, and the rest is up to the investor.

6. The Chance to Earn Long-Term Cash Flow for Decades

Many investors may choose to unwind their QOZ investments after a decade. But some may choose to keep their money growing tax-free through 2047. Not all funds, however, are structured to be held that long. Investors who hope to take advantage of this longer-term benefit must evaluate a QOF’s exit strategy and make sure they are investing in a QOF that will allow them to continue growing their investment tax-free through the end of 2047. At that time, all QOF investors will be required to wind down.

At Origin, we plan to hold the assets in our Qualified Opportunity Zone Fund III for as long as possible. We do that so investors can take advantage of long-term tax-free passive income and appreciation, when the Fund winds down. But it is impossible to know what market conditions will impact QOZ investments through 2047. Is it advantageous or necessary to sell a property to maximize profits or limit losses? This would affect an investor’s ability to use this strategy, which speaks to the risks inherent in all investment strategies.

Looking for Tax-Deferral Options Through Real Estate?

Bottom line, whether or not a QOZ investment is a good fit for a taxpayer’s investment strategies depends on several things. They include their financial goals, needs for liquidity, individual tax situation and tolerance for risk. It may be beneficial to ask to an investment advisor and accountant whether a QOZ investment meets their needs.

Are you interested in exploring other real estate investment strategies that help you defer taxes? Consider 1031 exchange services through Origin Exchange. And see how 1031 exchanges stack up as a tax-deferral strategy compared with Qualified Opportunity Zones.