A Message From Origin’s Co-CEOs Michael Episcope and David Scherer

We hope you had a chance to watch our webinar earlier this week with Sheila Bair, former head of the FDIC. She offered an authoritative perspective on recent bank failures, how individuals can protect their deposits, and broader implications for the financial sector. Also this week, the Federal Reserve approved its ninth consecutive interest rate increase, but the quarter-percentage-point hike and comments from Fed Chairman Jerome Powell appeared to acknowledge recent banking turmoil. In this week’s newsletter, both Dave Welk and Tom Briney address the future of the Fed: whether the agency will take into account the broader consequences of further rate increases going forward, and whether the responsibility of maintaining the health of the U.S. financial system reaches beyond the Fed and into the private sector.

Of course, the current environment has ramifications for the multifamily market as well. Here’s our take on where we believe there will be not just consequences but opportunities as well:

Lower loan availability. We believe that one consequence will be less lending in general. Banks will be less apt to extend credit because they’re worried about their own short-term balance sheets. The good news? That’s deflationary.

Undersupply in multifamily. Housing needs weren’t being met even before the economy encountered higher inflation and rising interest rates. Fewer loans equal less capital available for new housing developments—and the longer that shortage will persist. With strong long-term fundamentals in multifamily, this dislocation is an opportunity.

Pressure on refinancing. Dedicated lenders such as Freddie Mac, HUD and Fannie Mae will continue to be available to multifamily developers. But overall, there will be less money available to refinance debt. As a result, we believe real estate asset valuations will probably go somewhat lower.

New investment opportunities. Origin’s IncomePlus Fund is positioned to take advantage of the recapitalization market in the preferred equity space through the purchase of distressed properties, and the soon-to-be-launched Strategic Credit Fund is being designed to acquire preferred equity in multifamily assets. Preferred equity is currently being issued at 14%-15% today in protected positions even through stringent underwriting.

Potential for distressed investing. Origin’s expertise in restructurings, foreclosures, short sales, bankruptcies and gap capital during the Global Financial Crisis helped our Growth Fund I achieve a nearly 28% net internal rate of return. Currently, we don’t see distress yet, but we believe there will be dislocation by the end of the year, with potential opportunities to leverage.

The inverted yield curve has historically been a predictor of recession, and it’s too wide to ignore—along with the potential risks that could arise. We are being vigilant in our risk management strategies to protect our investors’ funds during this volatile period, even as we remain alert to the opportunities.

The Fed Finally Broke Some Things

The failures of Silicon Valley Bank (SVB) and Signature Bank, the second- and third-largest bank failures in U.S. history, respectively, represent one of the most turbulent periods in commercial real estate capital markets since the Global Financial Crisis. Much has been written about why these institutions failed; in SVB’s case, what broke many institutions during the previous crisis came home to roost.

SVB, the go-to bank for the tech industry, saw massive deposit growth in 2020-21. It couldn’t find assets as quickly as it was taking on liabilities, so it did what wound up cratering many financial firms in the earlier crisis—it mismatched long-term assets (U.S. Treasuries that lost value as the Fed raised rates) with short-term liabilities (deposits).

An imbalance in withdrawals forced SVB to announce a $2.25 billion capital raise on March 10. Word of SVB’s problems spread within the Twitterverse and, within 24 hours, $42 billion of deposits had been withdrawn, resulting in immediate failure and seizure by the Federal Deposit Insurance Corp. (FDIC). Signature, a bank affiliated with crypto investing, failed shortly thereafter, mostly on fears of a broader contagion among regional banks. While the FDIC guaranteed the deposits of these failed institutions, capital market participants that rely on regional banks—notably commercial real estate developers and investors—remain concerned about ongoing stability.

These events likely will lead to a few outcomes: First, more regulation of regional banks—likely through increased cash reserve requirements against deposit liabilities (read: less lending). This has a host of implications ranging from impacts to asset valuations and reductions in new supply to the increased importance of remaining debt capital providers. Second, less debt capital will lead to fewer transactions. The primary providers of development financing capital since market disruption emerged in 3Q 2022 have been local and regional banks. Over the past year, exposure to multifamily by commercial banks has increased substantially, equating to an increase of $118 billion over that period.

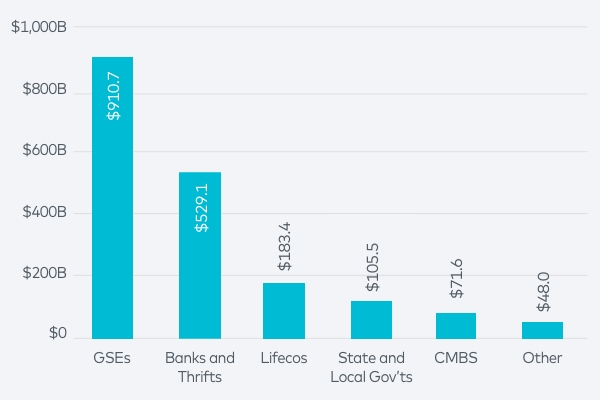

With a likely increase in regulations by the Office of the Comptroller of the Currency and the FDIC, who will fill the lending void left by regional banks that will be stockpiling cash? Life insurance companies (or “lifecos”), HUD, and low-leveraged or all-cash investors. Many large lifecos have construction financing programs that provide for conversion to longer-term “permanent” financing. Given their finite allocations, these lenders will likely become even more selective regarding the quality of projects and borrowers. HUD, a government-sponsored enterprise, or GSE, remains an interesting option for certain developers and borrowers; however, the additional time and cost to put a HUD loan in place must be considered. Lifecos represent only about 10% of the total outstanding multifamily debt market compared with banks and thrifts, at 29% (see chart below).

Mortgage Debt Outstanding

Sources: Newmark Research, Mortgage Bankers Association

Last year, HUD, as a subset of the GSEs, originated $5 billion for new development projects. Even with a likely uptick in lifeco production, these two sources would not come close to providing an equal backfill of the banks’ prior origination volumes. This could result in a decrease in the number of new projects in 2023 and 2024. Those reductions in supply could have reverberations on market conditions in 2025 and 2026, bolstering medium-term fundamentals.

For existing (non-development) properties, Freddie Mac and Fannie Mae allocations are similar to last year’s, with $150 billion in total production—resulting in some stability within this market segment. But a significant percentage of the $118 billion increase in bank lending activity to multifamily last year was to existing properties. With capped capacity from the GSEs and a reduction in bank lending, lifecos will not be able to carry the water here, which could precipitate an increase in low-leverage (via loan assumption or from conservative loans provided by active money-center banks) or all-cash transactions. Buyers using low or no leverage will require a higher rate of return for this inefficiency of their capital, which could lead to a further decrease in asset valuations.

As with any seismic shift within commercial real estate capital markets, these tremors will take months for the real damage to register. After these bank failures, the optimism and strengthening investor sentiment of earlier in the year has reversed course—and even before, investors were struggling to assess asset valuations due to a lack of available transaction data. This disruption will delay transaction activity and make these determinations even more difficult. I do believe and hope that the Federal Reserve will take the time to consider the broader consequences of further interest rate increases on capital markets when evaluating future monetary policy decisions.

Improving the Fire Department

I would like to start by saying I am grateful for the Federal Reserve System, the FDIC, monetary policy and now, the Bank Term Funding Program. This financial infrastructure is critical to national and global stability and deserves our full attention. With that in mind, I will point out the private sector has benefited from government intervention for more than a century, and it’s time for the private sector to give back.

The Federal Reserve System was founded in 1913 by the U.S. Congress to provide stability to our banking system, which had survived countless “bank runs” and payment suspensions since the First Bank of the U.S. opened in 1791. In 1933, in response to the collapse that led to the Great Depression, the FDIC was created to provide further comfort to depositors that their hard-earned savings wouldn’t disappear during a panic. Since then, there have been dozens of updates to the FDIC program, and the creation of multiple new tentacles of the Federal Reserve System, including the Fed’s discount window, the Federal Home Loan Bank, and, as of this month, the Bank Term Funding Program. All of it is working, for now, with liquidity coming in as needed (see chart). But, like our nation’s aging transportation infrastructure, our financial infrastructure is largely paid for by our government and could use the support of the private sector.

Fed Discount Window Borrowing

Source: Bloomberg

While the Federal Reserve System has adapted reasonably well over its 110 years of existence, it was designed in a time when newspapers were printed two or three times a day and information spread across the country over the course of days. Today, thanks to 24-hour news channels and social media, greater quantities of information—and misinformation—can cross the world in minutes. As former FDIC Chair Sheila Bair told us on Origin’s recent webinar, Fed policymakers tend to focus on “fighting the last war.” Now is the time to think ahead and prepare for solutions to problems that either don’t exist yet or haven’t been identified as problems yet.

The Financial Stability Board, a consortium of international monetary policy experts, took its current form in 2009 as a result of the Global Financial Crisis. It is the keeper of the list of Globally Systemically Important Banks, or G-SIBs. These are “too big to fail” household names such as JPMorgan, Bank of America, Citigroup, Credit Suisse and UBS—so critical that their collapse would put the entire financial system at risk. As a result, the world’s most powerful governments have implicitly pledged their balance sheets to backstop these banks in a time of crisis.

As tax-paying citizens of these governments, we should consider asking for something in return. I would like to see G-SIBs take a larger role in supporting the financial system in times of distress. Proof that this concept is possible is currently underway with several of the largest and strongest U.S. banks stepping in to support First Republic Bank. While there will certainly be mistakes made and inefficiencies in this process, having a permanent, implicit pledge of support for smaller institutions by G-SIBs is a reasonable form of payment for the implicit use of government balance sheets by those banks and would add further stability to the global financial system as a whole. Let’s take the next step and strengthen the fire department before the house is on fire.