In the world of real estate investment, financing ventures involve several parties with distinct roles. It’s not a simple cash transaction but rather a complex landscape that requires lenders, investors and stakeholders. Financing structures vary, each with their own advantages, risks and considerations. Mezzanine debt is often overlooked but highly effective. It can bridge gaps, unlock opportunities and facilitate growth in ways traditional lending methods cannot. This type of debt is commonly used when a company needs funding beyond what traditional senior lenders want to provide. An investor may assume the role of a mezzanine lender who provides capital to a business. In return, they receive interest payments and potentially an equity stake.

How Does Mezzanine Debt Work?

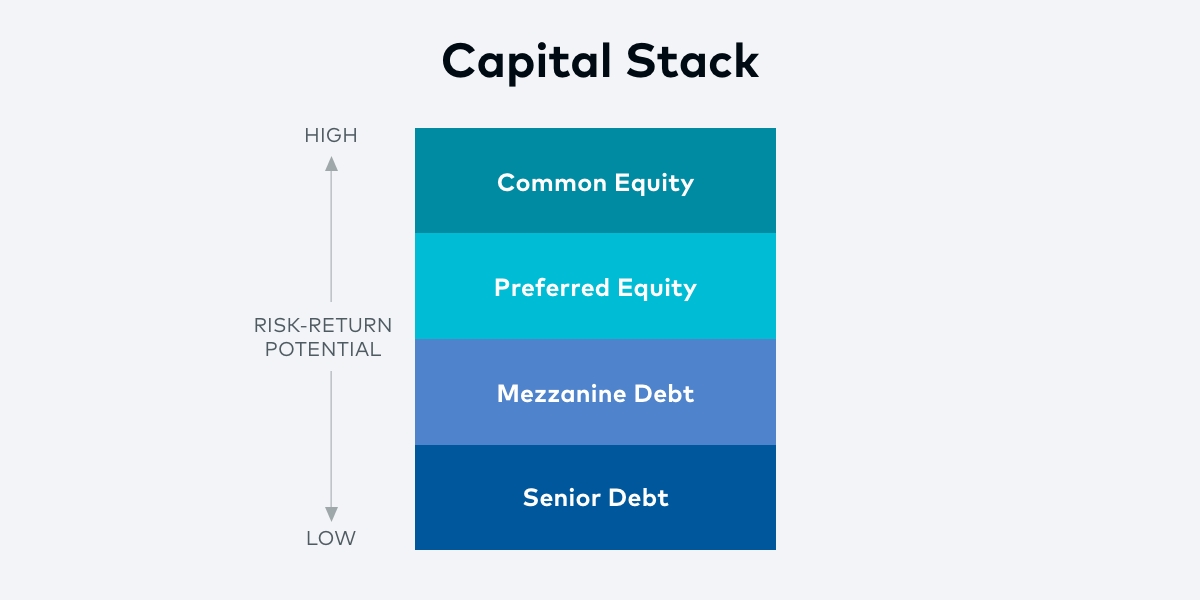

Mezzanine financing helps expand financing options and optimizes capital structure. It does this by providing an additional avenue for accessing capital beyond traditional debt and equity. It is often structured as a loan or a bond with certain characteristics of both debt and equity. In this way, it is providing a hybrid form of financing. It ranks below senior debt in the capital stack, meaning that in the event of default or bankruptcy, senior lenders are paid back first from the company’s assets. Senior debt holds the highest priority in repayment, granting it a superior claim over other debt in case of liquidation or bankruptcy. That makes mezzanine loans higher risk than senior debt. But because of where they sit in the capital stack, mezzanine loans have priority over equity owners in repayment.

Due to its increased risk, mezzanine financing generally carries a higher interest rate than senior debt. However, it offers greater potential returns. And it typically has a longer repayment period compared with senior debt. This type of financing may also incorporate an equity element, such as warrants (providing the lender the chance to buy a specific number of shares of the borrower’s stock at a predetermined price within a certain time) or an option to convert the debt into equity in the future.

A mezzanine loan typically has a defined exit strategy. It may be repaid through refinancing with senior debt, cash flow generated by the business, the sale of the company, or an initial public offering. Before providing a loan, lenders typically conduct due diligence on the borrower’s financials, management team, market position and growth prospects.

How Equity Differs from Mezzanine Financing

Equity represents ownership in a company, providing shareholders with the potential for profit and value appreciation. Equity financing involves issuing shares and granting control over decision-making. In contrast, mezzanine financing offers flexibility in repayment terms and customization. But generally, it doesn’t give the lender the same level of control over decision-making. Equity financing often funds long-term capital needs, growth initiatives, research and development, and strategic investments. Mezzanine financing frequently bridges a funding gap or finances acquisitions, expansions or other capital-intensive projects. The choice between equity and a mezzanine loan depends on factors such as need, risk tolerance and growth objectives.

The Benefits of Mezzanine Loans for Lenders

Mezzanine debt offers several benefits for lenders, including:

- Potential for higher returns: Mezzanine lenders have a higher level of risk compared with senior debt holders, this type of debt generally carries a higher interest rate than senior debt, as compensation for this increased risk.

- Diversification: Mezzanine financing offers lenders the opportunity to diversify their investment portfolios across a broader range of companies and industries, potentially spreading risk across various sectors.

- Cash flow and yield: Mezzanine loans provide lenders with regular income through interest payments. This can appeal to income-focused investors seeking stable cash flow.

- Potential equity upside: Mezzanine debt investments can include equity participation features such as equity warrants or conversion rights. If the company performs well and its value increases, mezzanine lenders can profit from that appreciation.

- Flexible structures: Mezzanine loan transactions can be flexibly structured to align with the company’s and the lender’s risk tolerance and goals for returns. Factors such as interest rates, repayment terms, security arrangements and negotiated provisions can be adjusted accordingly.

Risks and Considerations

While mezzanine loans can be a useful financing tool, they do carry certain risks. As mentioned, it’s a higher-risk investment compared with senior debt. And it is just as influenced by market conditions and economic cycles as other types of debt. Other risks include:

- Lack of collateral: Unlike secured debt, where lenders have a specific asset or property as security in case of default, a mezzanine loan relies more on the overall creditworthiness and cash flow potential of the borrower. This poses higher risk for mezzanine lenders. In case of default, recovering the outstanding amount becomes more challenging compared with secured debt.

- Complexity: Mezzanine financing can be complex due to their hybrid nature and the need to negotiate terms among multiple parties, such as senior lenders, equity holders and debt providers. This can pose challenges for lenders in assessing the risks and valuing investments.

- Illiquidity: Mezzanine debt investments generally tend to have longer investment horizons and lower liquidity than other investment options. Exiting such an investment before maturity can be complex, especially if there is limited secondary market activity for such debt.

- Prepayment risk: Mezzanine financing often offers call options or prepayment provisions, enabling borrowers to repay the debt before maturity. This can be disadvantageous for mezzanine lenders who may need to reinvest the proceeds at lower interest rates or rely on consistent cash flow.