When Will Construction Pricing Retreat?

Dave Welk, Managing Director of Acquisitions

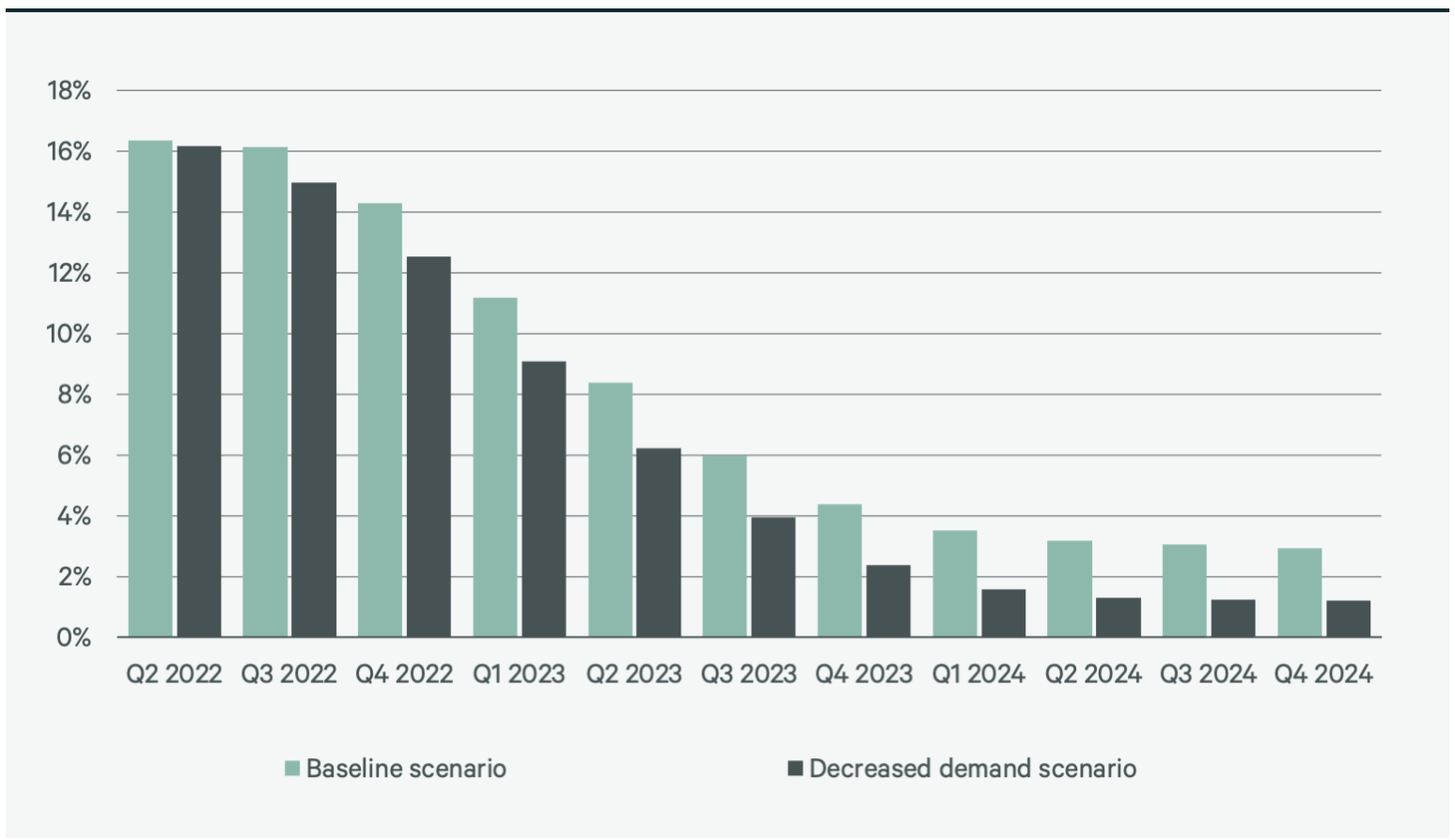

Given the rapid rise in apartment construction pricing since the start of the COVID-19 pandemic, developers and investors have been looking for signs of relief. According to CBRE Research, market participants won’t find any, at least for a little while. CBRE expects year-over-year costs to increase by up to 14% by year-end. This comes on the heels of two years of double-digit price increases, brought on by supply chain disruptions, labor shortages and increased construction activity within the single-family, industrial and multifamily segments.

In its forecast, CBRE notes that relief is on the way, with the escalation expected to stabilize in the 2%-4% range in 2023 and 2024, on par with historical averages. Significantly, CBRE made its forecast in July, when heightened demand for construction projects was expected to continue. In the chart below, the baseline scenario reflects CBRE’s outlook; we believe the reality will track more closely with the decreased demand scenario.

Average Annual Construction Cost Escalation, CBRE vs. Major Indices

Sources: BLS, Engineering News Record, Turner Construction, Rider Levett Bucknall, Mortensons, CBRE Cost Consultancy, CBRE Econometric Advisors, CBRE Strategic Investment Consulting, April 2022; via CBRE.

Over the past 60 to 90 days, we have seen a number of development projects hit pause throughout the Sunbelt and Mountain regions, for various reasons. One, noted in a previous Market Monitor update, is that regional banks and lenders are pulling back on construction lending. However, some investors and developers are re-evaluating projects that target top-of-market rents as cost escalations further squeeze profit margins.

Over the past 30 days, construction costs in a few of our projects have fallen compared to pricing obtained 60 to 90 days prior. The reductions, from 1% to 4% of total hard costs, were primarily in drywall, electrical and lumber materials. However, the aging skilled labor force is creating a scarcity factor and increasing labor costs could offset reductions in material savings. The use of technologies by subcontractors such as prefabrication in building and the use of virtual reality in worker training will likely be required to keep up with demand.

Given the observed slowdown in overall new multifamily starts next year, and the slowdown within the single-family sector resulting from mortgage rates in the 6%-7% range, we believe construction pricing will continue to retreat over the next year. While we will only underwrite these savings when contractually provided by our general contractors, these should offset the increased interest costs that we have had to include in the capitalization of our more recent deals.

The Search for Clarity

Tom Briney, Managing Director of Acquisitions

I have been having a lot of conversations lately, and the same question is being asked: When will the markets stabilize and return to some sort of “new normal”? My answer is always the same: The equity and credit markets will stabilize when there is clarity on the future actions of the Federal Reserve’s interest rate policy. The credit market’s bullish actions since the October Consumer Price Index (CPI) numbers were released on Nov. 10 is an indication that participants are seeing the fog of uncertainty lifting.

The government’s latest CPI reading for the trailing 12 months showed that prices of consumer goods had increased 7.7%. While that is still nearly four times the Federal Reserve’s target rate of inflation, over the following week the stock market increased 5% and the 10-year Treasury yield decreased by nearly 40 basis points. The response seemed to suggest that rampant inflation is a good thing. As anyone who has been shopping recently knows, rampant inflation is not good, it’s actually quite painful.

So why did the market celebrate? Because participants are seeing a movement towards clarity. The CPI peaked in June 2022 at 9.1% and has decelerated to the current 7.7%, a direct result of the Fed’s monetary tightening through both increased interest rates and (see chart) the shrinking of its balance sheet. As inflation appears to ebb, market participants believe they have greater clarity regarding future monetary policy—that is, that the Fed’s motivation to raise interest rates aggressively may wane as well. Federal Reserve officials, though, were very quick to state that it is not lifting its foot off the brake, which some perceived as negative but actually provides even more clarity for market participants.

Source: Board of Governors of the Federal Reserve System

With clarity comes stability, with stability comes recovery. While the country is still in the hospital, market participants are starting to see a path to getting healthy again.