In markets across the country, the COVID-19 pandemic has fundamentally shifted where we are spending our time. We believe these profound shifts will continue to produce a decrease in demand for real estate classes such as offices, lodging and retail. But, with many professionals now working remotely, individuals are placing more of a premium on their homes and apartments – and thus continuing the strong demand for multifamily real estate. As many of us reevaluate our current living situations, we’re also seeing renters flee highly priced coastal markets to relocate to more affordable suburbs or new cities entirely.

Here at Origin we’ve been investing in multifamily real estate for three decades, and we currently own or are in various stages of construction on 5,000 multifamily units across the country. We collect data from our multifamily portfolio that we compare to our competitors in each market, plus rely on national databases to augment our data sets and expand our benchmarks. Based on the data we’ve collected, we believe that multifamily real estate in non-coastal markets will be the highest performing real estate investment during this disruption.

A Look Back

In times of uncertainty, historical framing can be a helpful perspective. We’ve turned to data from the Great Recession of 2009 to use as a relevant frame to help determine what may happen in the real estate market today. In the chart below you can see multifamily total returns broken down by income and appreciation from 2005 to 2020. In this case, income means distributable dividends from operations, which increase returns and provide protection in a correction.

Multifamily real estate valuations from 2005 to 2020, including the Great Recession years, averaged a 7.98% compound annual growth rate (CAGR), but what is most notable is how quickly the multifamily sector regained the losses of 2009, and then followed with six consecutive years of double-digit returns. Although this data is a useful benchmark, we’d expect the Great Recession to have affected real estate more than what may happen to real estate during our current pandemic, because real estate and loans collateralized by real estate were at the center of the Great Recession, which is not the case today.

Data from Newmark Knight Frank Research, NCREIF. 2020 total returns are annualized.

Nice-to-Have vs. Need-to-Have

Over the past 42 years, multifamily also generated the highest average returns and also generated the highest return per unit of risk, as compared to other real estate asset classes (see charts below). This data should not be surprising, as housing is an essential need. In a recession, consumers cut back on travel, entertainment, and retail consumption, but housing is the last place they cut.

Furthermore, this year’s pandemic has created a world that places more value on the size and quality of one’s home or apartment. Many professionals are now working from home, and many places like coffee shops or bars are no longer viable as places to spend time working or socializing. Multifamily real estate has now also become essential for working and socializing. Real estate investors who can re-imagine their multifamily investments as multi-functional and develop new ways to serve residents’ expanded needs stand to gain during this time.

This data was pulled using historical returns from the NCREIF Fund Index – Open End Diversified Core Equity, which is a capitalization-weighted, gross of fee, time-weighted return index that typically reflects lower risk real estate investment strategies utilizing low leverage and generally represented by equity ownership positions in stable U.S. operating properties across regions and property types.

What Rent Collection Data Shows

A frequent question we receive from potential investors is how can renters pay their rents when the unemployment rate is so high? But rent collection data thus far shows that renters have proven to be more resilient than expected. The National Council of Real Estate Fiduciaries reported April 2020 collections at 91.7% and June 2020 collections at 93.1%. The National Multi Housing Council reported that 94.6% of rents were collected in April 2020 and 95.9% in June 2020. To put that in perspective, in 2019 rent collection averages were 97% to 98%.

At Origin we have collected 94.5% of rent from April through July 2020. We do, however, see a divergence between our Class A and Class B properties. Class B properties are averaging 89%, while Class A properties average 97%. We believe this is due to the higher savings of the Class A renter, as well as their ability to work remotely. Many of our Class B renters have seen their jobs in retail, service and hospitality affected greatly by the pandemic. We believe that this is a short-term disruption and the government stimulus has been helpful.

Occupancy and Rate Data Holds Strong in Non-Coastal Markets

Collecting rent is nice, but at what occupancy and rate? According to RealPage, the average multifamily occupancy rate has remained robust at 95.7% nationally. We have seen an uptick in the occupancy of our multifamily portfolio, with particular demand in Dallas, Austin, and Phoenix. Nationally there has been a trend towards higher occupancy and rent amount charged in non-coastal cities.

Rents were down 1% in the second quarter of 2020 nationally, but the dichotomy between coastal and non-coastal cities is stark. Many of the coastal cities were highly priced and renters are now opting to relocate to more affordable suburbs or new cities entirely. At Origin, we selected our 11 target markets taking into consideration business desirability, lifestyle, and affordability. Six of our target markets in particular: Nashville, Denver, Phoenix, Charlotte, Atlanta and Austin are benefitting from the demographic moves caused by COVID 19. The data has us confident in our strategy to continue investing in non-coastal markets.

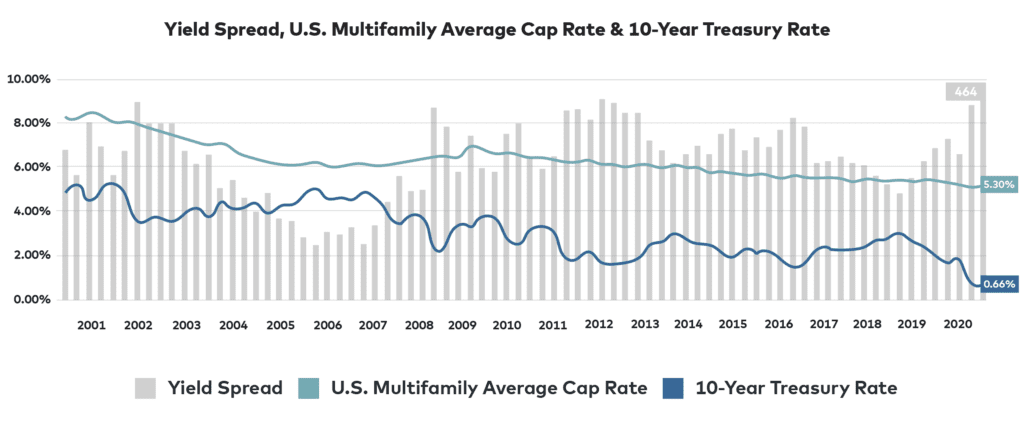

Debt is Cheap

By any measure the borrowing costs to finance real estate are currently low, which increases returns to real estate investors. Variable rate loans are currently priced over the one-month LIBOR rate, which currently is .16%. Prior to the pandemic LIBOR was 1.75% to 2%. The ten-year note yield is currently .68% and the spread between the ten-year yield and capitalization rates is over 450 basis points. Importantly, borrowing rates for multifamily real estate have also declined, as Fannie Mae and Freddie Mac have outpaced their 2019 levels of loan issuance in April, May and June of 2020. Borrowing costs for stabilized real estate are below 3%, and often go as low as 2.5% at leverage below 60% loan-to-cost. This is important, as investment returns benefit when borrowing costs are lower than the stabilized capitalization rate.

Data from Newmark Knight Frank Research, Federal Reserve Bank of St. Louis, Real Capital Analytics.

Multifamily Valuations

Despite the pandemic, we haven’t seen much volatility in multifamily real estate valuations. We’ve tracked all institutional sales of multifamily assets in our 11 target markets since the beginning of the pandemic. We’ve witnessed 90% of the sales over the past five months occurring at pricing that was flat with February 2020 (pre-COVID-19) pricing or within 2% of that pricing. Real Capital Analytics has also reported only a 4.9% correction for multifamily real estate in non-coastal markets thus far. With interest rates remaining low we expect the valuations of multifamily real estate to remain solid.

Like us, we’ve seen that the market continues to believe in the power of multifamily real estate as an asset class. We believe that high demand for multifamily assets, both from renters and from investors, paired with low interest rates create the likelihood for strong performance in multifamily real estate investing over the next three to five years. At Origin, we continue to explore opportunistic multifamily asset purchases and expect to continue investing in multifamily real estate in our 11 non-coastal target markets.