Balancing an investment portfolio means finding the right mix of risk and reward. Public real estate investment trusts (REITs) and private equity real estate can both offer higher yields and may lower a portfolio’s overall volatility. Either one will enhance a traditional portfolio of stocks and bonds. So which is the smarter choice—public REITs or private real estate? New research shows they’re better together in an investment portfolio.

As indirect ways to own property, REITs and private real estate have a lot in common. Both can offer investors a buffer from the ups and downs of other equities and provide passive income. Nuveen recently assessed real estate’s income and diversification benefits and found real estate yields in the U.S. have outpaced inflation since 2013 and have now pulled much farther ahead. While private real estate shows lower absolute returns than public REITs over the past 20 years at 9.2% vs. 9.6% respectively, prices of both assets follow the broader real estate market.

However, public REITs are a more of a leading indicator of the broader real estate market than either direct investments or private real estate funds. When market conditions change—for instance, when competition makes it harder to raise rents—public REIT asset values are first to reflect the new conditions. Shares can be bought and sold immediately, often based on investor sentiment alone, and that can produce wider price swings. So, depending on market conditions, a REIT’s stock price can be substantially higher or lower than the valuation of the underlying real estate—even as the passive income it pays investors in dividends remains the same.

By contrast, a change in capitalization rates in private real estate won’t immediately be reflected in property valuations because buildings first have to be marketed, appraised, underwritten and sold before market conditions are represented in the price. So private real estate returns show this tempering effect as net asset values are priced to current market conditions only periodically and with a lag.

Safety in Numbers: Diversify Portfolios With Both

Adding either form of real estate may improve the performance of a stock and bond portfolio. The Nuveen study calculated 20-year returns on a mix of 55% stocks, 35% bonds and 10% real estate. Either 10% public REITs or 10% private real estate produced better returns than with a 60% stock, 40% bond split.

Notably, real estate with contractual lease income and the potential to increase rents over time gives both public REITs and private real estate values a low correlation with stock and bond prices. In fact, Nuveen found a negative correlation between bonds and private real estate, meaning their prices tended to move in opposite directions.

Public REITs tend to show higher total returns than direct real estate investments, but with more market volatility—a bigger spread between high and low results, and thus a greater risk of loss. Private real estate, because of its lower volatility, produces higher risk-adjusted returns.

But there’s a happy medium. Nuveen tracked a third portfolio with the same real estate allocation but with 80% allocated to private real estate and 20% to public REITs, or 8% and 2% of the total portfolio. With this allocation, 20-year returns had better risk-adjusted returns than the all-REIT or all-private options.

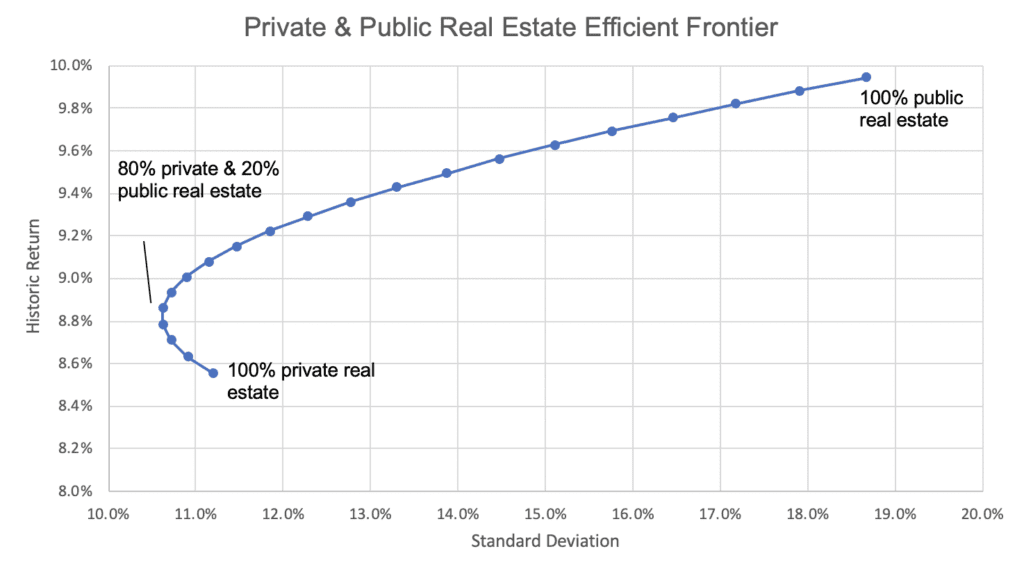

Is this the best possible asset mix? Using the same methodology, we diagramed the entire range of allocations for risk vs. reward, from 100% listed REITs to 100% private real estate funds, and calculated the Sharpe ratio (which measures the performance of an asset compared to a risk-free asset such as Treasury note or similar low-risk option) for each. The mix with the highest Sharpe Ratio, comprised 79% private real estate and 21% public REITs. That doesn’t make 80/20 the best allocation, it just produced the best risk adjusted return.

REITs Customize a Real Estate Portfolio

Future returns could fall on either side of the line on this chart, but the historic averages along this “efficient frontier” suggest the steadying role that public and private real estate together can play in a portfolio. A mix of public and private real estate could potentially achieve the same returns as private alone but with lower risk. Yet adding more REIT to the mix could improve expected returns, albeit with greater market volatility. The choice depends on the investor’s target rate of return and risk tolerance.

But there are other advantages to holding public REITs in combination with private real estate funds.

Since REITs are publicly traded, liquidity is an important benefit to owning them. They can be held short term or long term and generally have higher dividend yields than money market rates. Selling shares will make cash immediately available for buying a house, paying college tuition or any other planned purpose, including future capital calls for private equity commitments. Public REITs also can also be used to optimize sector allocations within an overall real estate portfolio. An investor that has a lot of exposure to multifamily in a private real estate fund might look to REITs that own other property types. And it might take a combination of REITs to get a certain asset mix.

In the short term, public REITs trade more like stock market equities, which go up and down daily, while private real estate prices are sticky and slow moving. But there’s no need to choose one or the other. Private and public together is a pairing like peanut butter and chocolate. Either is good by itself, but the two are a great combination, a whole that’s greater than the sum of its parts.