The Death of the Fed Put

Tom Briney, Managing Director of Acquisitions

The “Fed put” isn’t listed as an official policy in any Federal Reserve documents, but it is a widely accepted, and more recently, embraced idea by financial market participants. The concept, based on the action of a put option, suggests that the Fed will step in to stabilize financial markets if asset values fall too quickly or too far. The Fed confronts these very subjective measures of instability with a quiver of tools including lower interest rates, bond purchases and repurchase agreements. The Fed put really took shape during the global financial crisis of 2008-10 and has increased in frequency and magnitude in recent years.

Many of us are old enough to remember where we were when Lehman Bros. collapsed and CNN was airing images of newly unemployed investment bankers walking down Wall Street with boxes of personal belongings. This event set the stage for the first massive Federal Reserve intervention in modern history and the playbook for the concept of a Fed put. From 2008 to 2010, the Fed injected more than $2.1 trillion of liquidity into the financial system, providing a floor in asset values, liquidity in the markets, and just enough confidence to get market participants off the sidelines. Fed interventions in 2016, 2018 and 2020 cemented the concept of the Fed put.

Subscribe

Subscribe to receive the latest articles about fund updates, industry news and market trends.

We’re all familiar with the legal warning that “historical performance is not an indicator of future results.” This time is different, and today’s market participants would be wise to consider this in today’s context. The underlying cause of the fire currently being battled by Chairman Jerome Powell and the Fed is an overheated economy. To get a fire under control, one must remove oxygen, fuel or both. Since early 2022, the Fed has been working both angles by increasing interest rates and selling bonds, which so far has been effective only in containing the spread of—but not controlling—the fire.

If financial markets destabilize further, in the form of job losses, increased unemployment or further declines in asset values, the Fed will not intervene with lower interest rates or more bond purchases. This additional instability is their goal: lower employment, create job losses and reduce asset values—effectively, bringing the fire under control, without extinguishing it. It is the Fed’s hope that this incremental instability happens in a controlled manner, and without creating a recession—extinguishing the fire—but, as reaffirmed in multiple interviews, Powell’s goal is far more important to him and the Federal Reserve than their hopes. The Fed put is dead.

It is our belief at Origin that one shouldn’t stop investing because of market conditions. Rather, investors should put themselves in the best position to be successful given current market conditions. This includes not fighting against the Fed but alongside it, by buying floating-rate debt and investing in preferred equity. These strategies are defensive in nature and limit the chances an investor will be burned by the economic fire and the ensuing economic instability.

S&P 500 and Federal Reserve Intervention

Source: Advisor Perspectives

Silver Lining in Rent Declines

Marc Turner, Managing Director of Investment Management

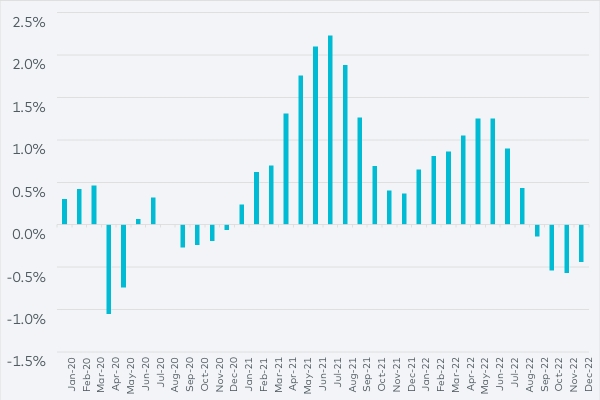

Apartment rents across the U.S. recorded a fourth consecutive monthly decline in December, signaling a further cooling in the U.S. housing market brought on, in part, by the Federal Reserve’s tightening monetary policy.

According to RealPage Market Analytics, effective asking rents for new leases nationally fell 0.44% in December, following an average erosion of 0.28% from September through November 2022. Rents fell 0.59% in November, the largest monthly decline since 2010, outside of the pandemic-distorted months of April and May 2020.

Change in Effective New Lease Asking Rents, U.S. Market Rate Apartments

Source: RealPage Market Analytics

On a year-over-year basis, RealPage data shows that national effective rent growth for new leases was 5.68%, the smallest increase since May 2021 and well below the peak of 15.7% in March 2022. Occupancy in December remained relatively high at 94.95%. That’s consistent with long-term averages, and slightly below the same month in both 2018 and 2019, but 2.53% below December 2021. Leasing traffic among prospective renters declined throughout 2022, and Q4 2022 activity was the weakest for any fourth quarter since 2014, which itself was about 14% below the 10-year historical average.

The silver lining here for multifamily investors and operators is that resident turnover remains historically low: Average turnover in Q4 2022 was the second-lowest recorded by RealPage for any fourth quarter over the past 10 years, bested only by Q4 2021. That’s good news for operators and owners because it means money isn’t being spent on marketing to potential renters and unrented spaces aren’t sitting empty. And during a recession, it’s even more important to maintain cash flow through retention.

Speaking of which, many economic observers are predicting a recession this year, including us—we see it likely happening by October. With that threat looming, consumer confidence has weakened—and that, coupled with lower household formation, has led to lagging demand for apartments. The University of Michigan’s consumer sentiment index in November was 15.7% below the year-earlier period, a decline more severe than the change in attitudes seen during the Great Recession. However, according to the university, “extremely negative attitudes have softened on the basis of easing pressures from inflation.” And the December index shows an improvement of 5.1% over the November survey.

Another glass-half-full view, though, is that inflation appears to be losing momentum. Month-over-month inflation numbers from June to December 2022 slowed significantly to around 2.64% annualized, almost back down to the Federal Reserve’s 2% target rate. There may be a seasonal skew in these results, and months of good news aren’t likely to convince the Fed to back off on its aggressive interest rate moves just yet; however, there are reasons for optimism.

We have expected this deceleration in rent growth—and have predicted a retreat into negative territory—including factoring it into our underwriting and due diligence. Although near-term challenges exist, we believe strong fundamentals for multifamily demand remain positive in the long term, even if 2023 is shaping up to be a bumpy ride.