Are Office Loan Maturities the Next Iceberg for Regional Banks?

Well, another week and another regional bank failure. When the sun rose Monday morning, reports broke of the Federal Deposit Insurance Corp.’s seizure of First Republic Bank and subsequent sale to JPMorgan Chase over the weekend. It is the second regional bank with more than $200 billion in assets to fail in as many months, with similarities to Silicon Valley Bank and Signature Bank—losses stemming from mismatching durations of assets and liabilities and a run by fearful depositors.

These banks failed primarily because of balance sheet issues and not necessarily due to bad or risky loans. But how will other regional banks fare that have similar balance sheet issues and a large exposure to struggling office loans within their portfolios? Further, how could these issues impact available credit for commercial real estate sectors, that may be relatively healthier (such as multifamily and industrial)?

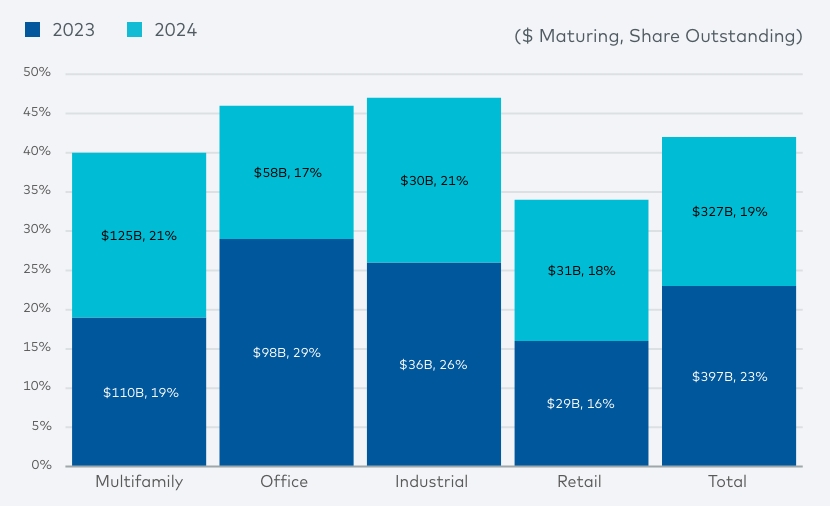

Following up on my most recent Market Monitor article, to assess these risks, we’ll take a deeper dive into office exposure in the banking system. According to the Mortgage Bankers Association, as ofQ3 2022, the commercial and multifamily debt market totaled approximately $4.5 trillion. Banks and thrifts accounted for approximately $1.7 trillion, or 38% of the total. Over the course of this year and next, roughly 42% of this total will be maturing. Of that, $156 billion of bank-originated office loans will mature, about 9.1% of all commercial mortgage debt outstanding and 46% of all office loans outstanding.

Bank Loan Maturities, by Property Type, through 2024

Source: Mortgage Bankers Association, as of March 2023

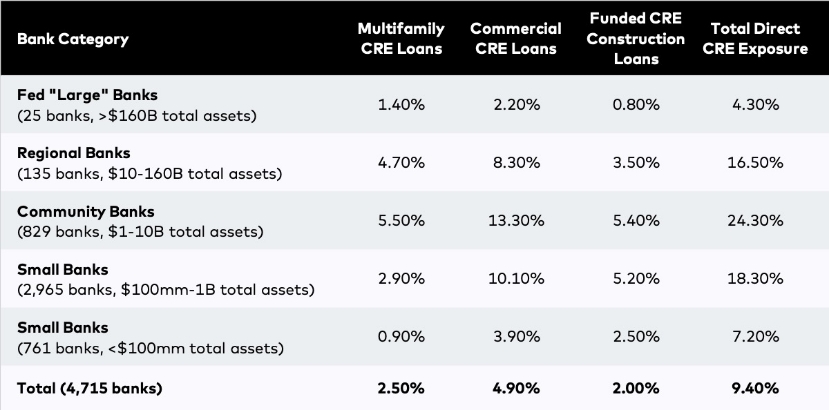

The analysis gets more interesting when you review where this risk is concentrated. The exposure to real estate loans as a percentage of total assets is highest among community banks, at 24%, but among the largest U.S. banks, it’s only 4.3%. To provide some perspective, within the insurance industry, where maturity risk concerns largely have not been raised, exposure to real estate loans is about 8.3%, with some at or above 20%.

Wells Fargo, for one, is sounding the alarm bell. During its first-quarter earnings call—and despite its relatively modest exposure to commercial real estate loans—the nation’s largest commercial real estate lender announced that it would increase its loan loss reserve by $643 million. That is largely to address potential losses within its office portfolio, which represents 25% of its commercial loan portfolio. Large, heavily regulated banks such as Wells Fargo and PNC Bank—which reported that its office exposure is limited to 2.7% of its $36 billion loan book—can withstand their limited exposure to commercial real estate. But the small, community and regional banks face a bigger struggle with their own maturing office loans.

Share of Bank Assets Exposed to CRE Loans

Source: FDIC, Moody’s Analytics

Taking note of these risks, Moody’s Investors Service downgraded 11 regional lenders recently, citing, among other items, increased exposure to commercial real estate losses. The downgraded lenders are U.S. Bancorp, Zions Bancorp, Bank of Hawaii, Western Alliance Bancorp, First Republic Bank, Associated Banc-Comerica Inc., First Hawaiian Inc., Intrust Financial Corp., Washington Federal Inc. and UMB Financial Corp.

While these downgrades appear to portend storm clouds for a number of other regional lenders, historical context from a recent JPMorgan analysis is helpful. “Applying historical loss rates drawn from the GFC (Great Financial Crisis) to office and retail holdings only, the impact in (commercial real estate) would likely not rise to the level of a capital event for the banking industry.”

While office fundamentals are structurally impaired, retail fundamentals are more favorable now than when the GFC began, providing additional room for office loan losses in the event that they increase beyond historic highs. At this point, it does not appear that office-sector loan losses will break the regional banking system.

That said, we anticipate that many regional banks will continue to come under additional regulatory scrutiny and be forced to further shore up balance sheets, notably through reduced lending to otherwise relatively healthy property sectors. We expect to see a slow unwinding of office loan exposure by banks as the $156 billion of bank loans matures over the next two years. There will be significant negotiations between borrowers and lenders that do not wish to exercise their rights of foreclosure to take on ownership, management and, ultimately, a write-down of assets. Some office transactions will be sold at or below land values. Examples of this already exist in the marketplace and will pick up momentum as the regional bank lending market looks for stability in the coming months. We are looking at larger, healthier banks to fill some of the void left by smaller peers to keep the multifamily development capital spigot flowing.