We began 2022 in a much different place than we are completing it. At the end of 2021, assets were riding high and the Federal Reserve believed that inflation was transitory. Now, two weeks from the end of 2022, we’ve seen inflation hit a 40-year high and multiple interest rate increases pummel the lending environment. What does that mean for multifamily in 2023?

We moved into new economic territory this year, but it isn’t totally unknown to us. Last year, we made some predictions—about pernicious inflation, rising interest rates, cooling multifamily values—that proved prescient. But we didn’t just write about it. We did something about it, from hedging interest rates, adapting our Funds to remain resilient and leveraging economic forces to our advantage. Our Funds are performing today because of the actions we took early on.

There are a lot of unknowns coming in 2023, but I can provide some perspective on how I believe it will unfold. Here are my top 10 predictions for 2023.

1: A recession is coming.

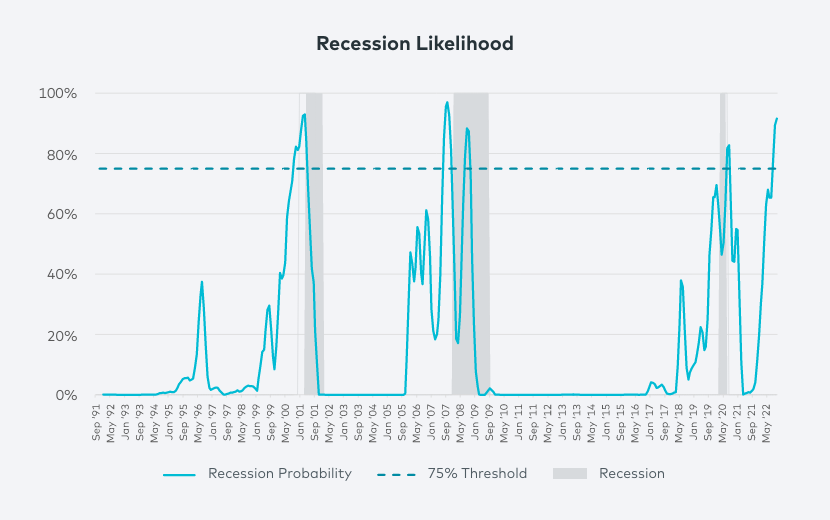

There will be a recession in 2023, and it will be quite different than the brief one we experienced when the COVID-19 pandemic stopped the global economy in its tracks. I’m not alone in predicting a recession, of course, but I’m willing to mark the calendar on the approximate timing: According to Origin’s proprietary suite of machine-learning models, MultilyticsSM, there is nearly a 100% likelihood of a recession occurring by October 2023. At Origin, we have been preparing for a recession for a while and taking steps to mitigate its impact in several key ways.

We have relied on Multilytics to predict rent growth as we evaluate deals and future opportunities in the market. While Multilytics can predict the likelihood and timing of a recession, however, it can’t foresee its length or depth. Rather than a brief dip into recession territory as we saw in 2020, I believe we will be swimming closer to the deep end—not quite as deep as the Great Recession, but a serious downturn without a soft landing.

Source: Multilytics

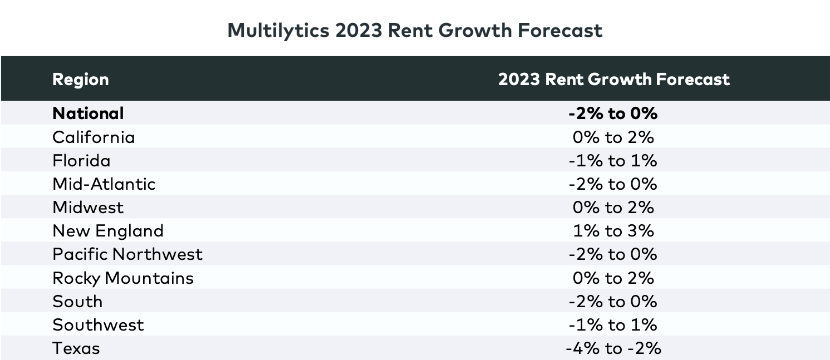

2: Multifamily rents will enter negative territory.

Multilytics predicted that strong rent growth for Class A buildings would last through the first half of 2022 and then begin to flatten. It’s telling us that in 2023, in more than half our markets and submarkets, that negative rent growth will occur. In multifamily real estate, this is a consistent warning sign of a recession. Also, forecast deliveries of new apartment units in 2023 will put further downward pressure on rents. We are seeing this in our own target markets and elsewhere.

Source: Multilytics

Rents have grown by double-digit percentages for two years in a row, and salary increases haven’t kept pace, either with those increases or the jumps in inflation we’ve experienced. While multifamily investors have been reaping the benefits, particularly in high-growth areas, I believe that a correction is necessary and that it will set us up for long-term health in this asset class.

For most of the past year, we have been underwriting deals that anticipate 0% rent growth in Q4 2022 and negative rent growth next year. If our models predict negative rent growth but we still meet our cost of capital, we can choose to do a deal. The companies that bought real estate at inflated prices last year are relying on continued rent growth to remain profitable, and I don’t think they’re going to get it.

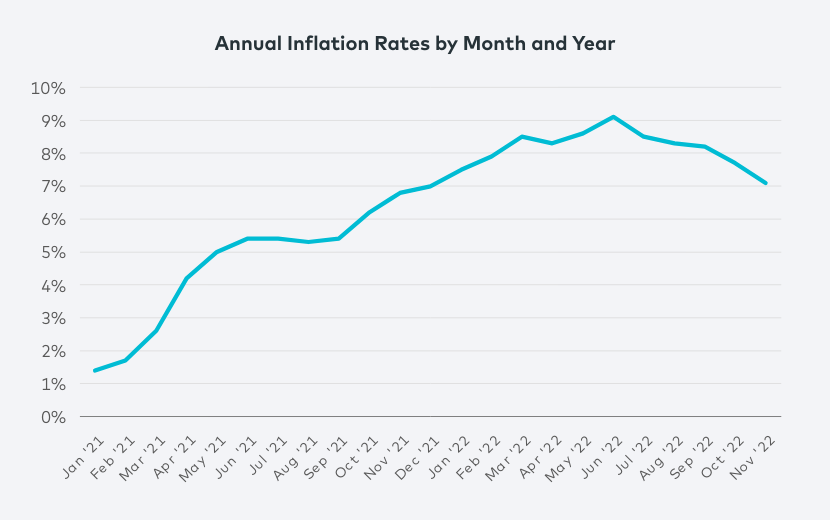

3: Inflation has peaked and will decline to around 4.5%.

Last year I predicted that inflation would stick around. And it has remained stubbornly high, clocking in at 7.1% in November. I’m predicting that it will move to about 4.5% over 2023, with a caveat (see prediction number 4).

Predictive indicators of inflation, such as commodity indices and the New York Fed’s supply chain pressure index, are easing, and the shipping container backlogs that peaked earlier this year have disappeared. Specific commodities like lumber, which topped $1,300 early this year, are now trading in the mid-$400 range. And, as we discussed above, flattening rent growth is impacting inflation as well—that’s significant because 30% of the Consumer Price Index comprises housing costs.

4: Wage inflation will persist.

During the past year, we’ve seen a low unemployment rate combined with big imbalances in the labor market: Tech companies like Microsoft, Twitter, Meta and Amazon are downsizing by the thousands after years of unprecedented pandemic-era growth. Wall Street firms are doing the same with hundreds of employees as financial activities slow relative to 2021. Those losses, though, are dwarfed by demand in blue-collar and service-sector industries, and workers at companies such as Starbucks and Trader Joe’s are driving to unionize.

When wage inflation starts, it’s hard to stop: While the definition of “tight labor market” varies, wages and salaries increased 5.1% for the year ended September 2022 and 4.2% for the year ended September 2021, according to the U.S. Bureau of Labor Statistics. I see it as a good thing for society, but it will keep inflation lingering.

5: Interest rates will keep rising.

In 2022, we have watched interest rates climb aggressively to mitigate the effects of 40-year inflation highs. The U.S. Federal Reserve chairman recently indicated that the pace—if not the size—of the increases will slow in the coming year. I think the Federal Funds rate, which guides overnight lending rates, will continue beyond its current 4% or so up to at least the 5%-to-5.25% range, sending 30-year mortgage rates north of 8%. All this puts enormous pressure on the housing market, not just owned homes but the rental market. As long as inflation persists at the wage level, interest rates will remain high in 2023.

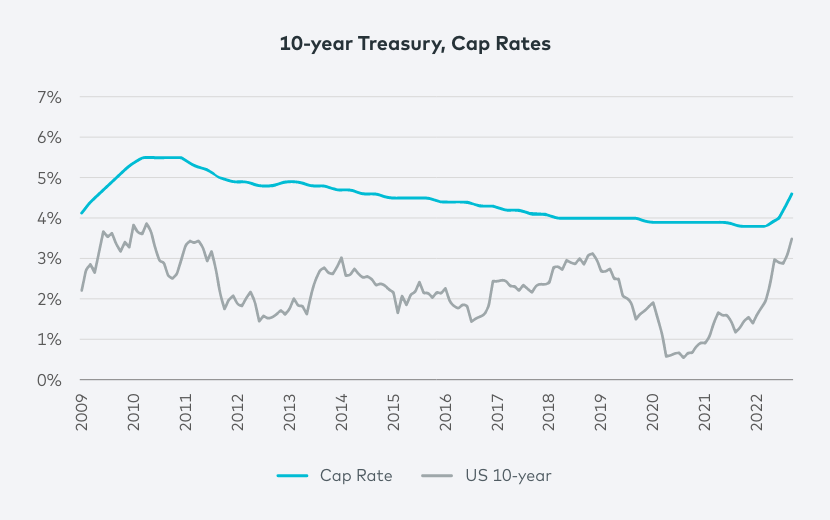

6: Cap rates will go higher.

At the end of 2021, cap rates were moving in the 3.3%-to-3.5% range. They’re currently hovering around 4.25% to 4.50%. That 100-basis-point increase is outmatched by borrowing costs, which have increased by 250 basis points over the same period, creating negative leverage depending on the deal.

This isn’t sustainable, and there are two possible ways forward. One is that borrowing decreases and cap rates don’t need to move; another is that cap rates increase enough to overtake borrowing costs—but we already know that any increase in cap rates won’t be due to rent growth.

As this situation sorts itself out over the coming year, another disparity will emerge: Responsible investment managers will prove themselves and cherry-pick the best opportunities, and over-levered ones will be scrambling and selling. That leads, unfortunately, to my next prediction.

Source: CBRE through 2020, 2021-2022 are estimates based on the data provided by CBRE

7: Distress is coming to the market.

In 2021, low interest rates combined with other factors to incentivize overpaying for value-add and ground-up multifamily properties at double-digit percentages over replacement costs. Some of those deals used debt fund capital in their financing. At the time, it made sense (to those buyers, anyway) because they had strong positive leverage. It hasn’t made sense to us to take similar risks—we haven’t bought an existing, rent-producing building in about two and a half years.

As interest rates have risen and rent growth has cooled, the leverage of those overenthusiastic buyers has shifted, as well. Those projects will refinance their debt with more conservative lenders. I believe we will start seeing signs of distress in the second half of 2023.

Our Funds are defensively positioned and we are insulated from these types of issues. But we’ll be able to play offense if this probability transpires.

8: Opportunities for investors will emerge in preferred equity.

I’ve said that in the next 12 months, multifamily rental rates will experience negative growth. So why should someone invest in this asset class before 2024? The opportunities for the next six to 12 months will be in preferred equity because they are well-protected positions in the capital structure. As well, over the next 12 months and into 2024, a window of opportunity will open to buy assets well below replacement cost and at reduced prices as distress starts to emerge.

9: The build-for-rent segment will boom.

Build-for-rent (BFR) housing, a category of low-density single-family or townhouse-style rental community, is developing big momentum as demographics shift and interest rates keep prospective buyers out of homeownership. As new households form that include more work-from-home employees, older empty nesters and younger families with children, these groups can find housing with several bedrooms, larger floor plans and yards in the BFR space.

The number of units being built this year increased 106% compared with a 36% increase in 2021, according to home improvement site Fixr. The pace of BRF starts is expected to pick up to 180,000 units by 2025. We are invested in this adaptable, spacious approach to multifamily housing, and we’re bullish on its future.

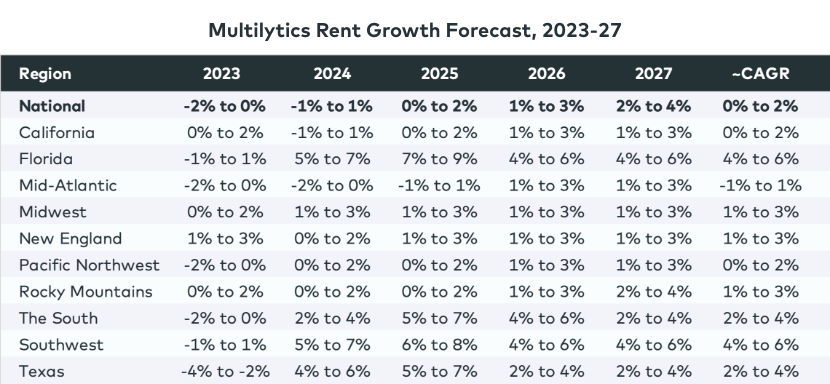

10: Multifamily fundamentals will gain momentum in 2024.

I know that predictions 1 through 9 are a mixed bag. But I want to end on an encouraging note: Multifamily housing will move through negative rent territory in 2023. Longer term, though, Multilytics shows that trend generally reversing in 2024 into positive territory in 2024. And in 2025, 2026 and 2027, it’s quite strong.

Source: Multilytics

This isn’t just wishful thinking. It’s true that multifamily construction starts will slow over the coming year as the result of rising construction costs, cap rates and borrowing rates. But the U.S. is underhoused by up to 4 million units—depending on which study you look at—a problem exacerbated for years by the Great Recession. This shortfall isn’t going to go away.

The bottom line: As an asset class, multifamily is difficult to disrupt—and you can’t live in the metaverse. Multifamily housing will withstand any disruptions that the next year brings and rent growth will re-emerge as demand returns.

Previous predictions: If you’d like to see what I’ve predicted in years past, you can check out my predictions for the following years: 2022, 2021, 2020 and 2019.