The Origin IncomePlus Fund is our flagship private real estate investment vehicle and its portfolio has been purposefully designed with both preferred equity and equity investments so we can deliver high risk-adjusted returns across all market cycles. As an active manager of private real estate, it is our job to make tactical moves across our portfolio that are consistent with the opportunities we see in the market. In a growing market, a portfolio made up of all equity investments is optimal as this investment has unlimited upside. In a declining market, preferred equity is the more favorable investment choice because it generates a far more stable return with downside protection. Understanding where we are in the market cycle is the key to successful active management.

In today’s market, we’ve seen economic fundamentals deteriorate without much change in the corresponding price of real estate. This means that either the fundamentals need to catch up to price or the price needs to come down to match the prevailing economic conditions. In any case, acquiring equity investments in the current pricing environment is likely to generate low absolute returns for the next 12 to 18 months until these two opposing forces find equilibrium. We don’t have a crystal ball to know exactly how this will play out, but we do understand the difference between price and value, and know what a good risk-adjusted return looks like. In any market, the best risk-adjusted returns can be found where there is an imbalance between buyers and sellers, and the pandemic has created an opportunity for preferred equity as lenders have pulled back and tightened their standards.

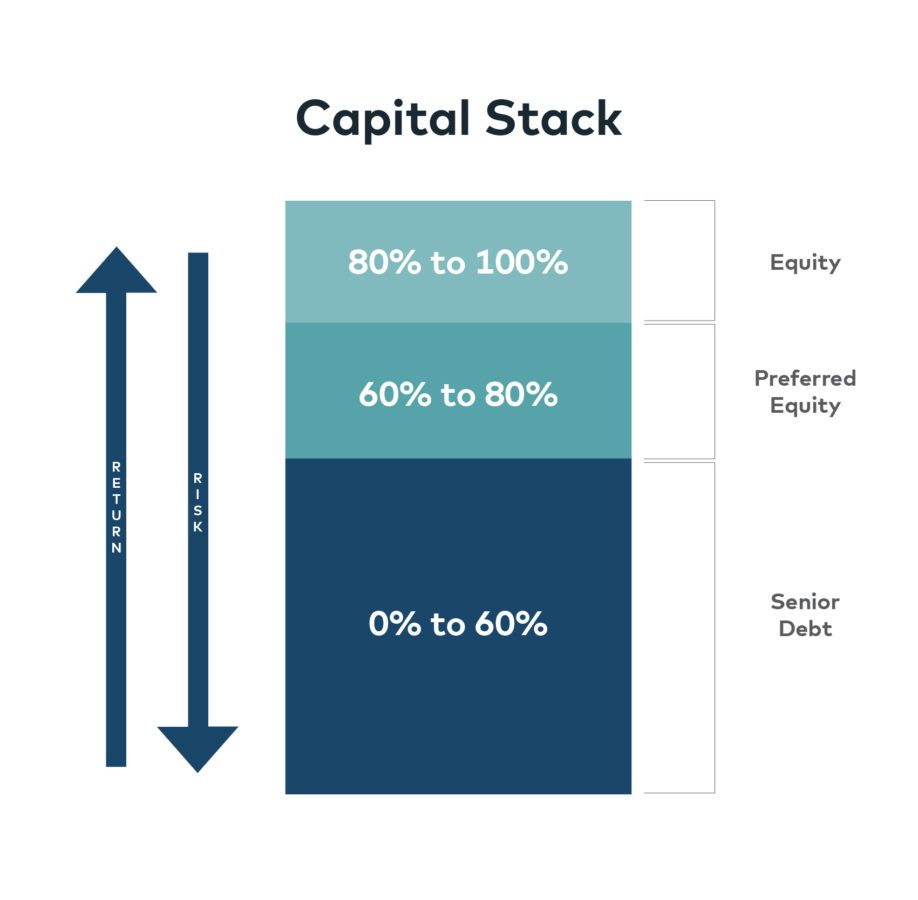

What is Preferred Equity?

Preferred equity sits between debt and equity in the real estate capital stack and is a hybrid of both, enjoying protections similar to those of a senior lender, but receiving returns equivalent to an equity position, about 12% to 14% annually. Late last year, we began to intentionally tilt the IncomePlus Fund’s target makeup towards preferred equity investments as property prices began to exceed values, which significantly helped to cushion the impact of the COVID-19 pandemic. Preferred equity has always been a critical component of the IncomePlus Fund’s strategy as it provides capital protection, yield and price stability. The need for this type of capital has never been greater as banks have left a gap in the capital stack.

IncomePlus Fund’s Target Portfolio

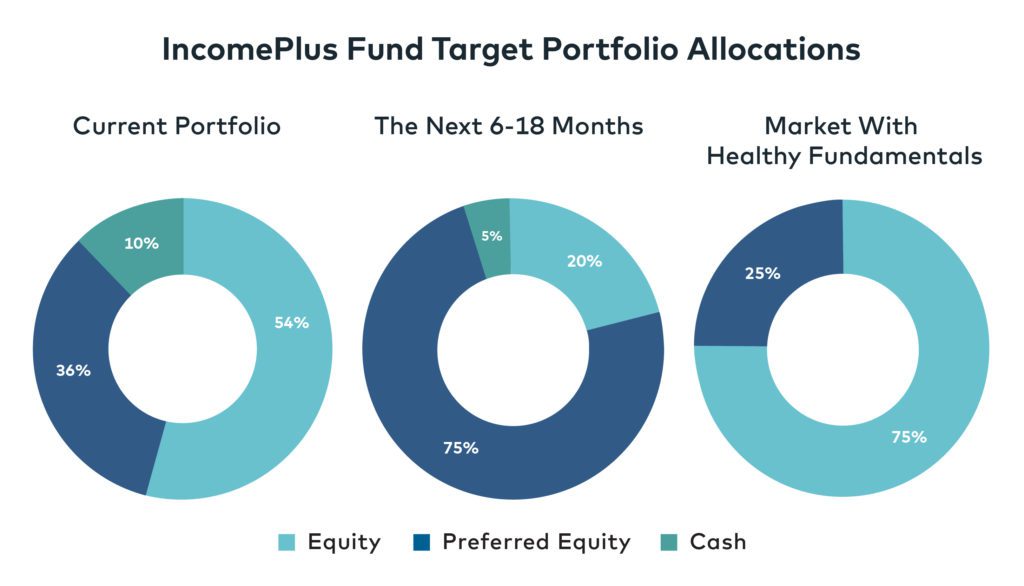

In a normal real estate market with healthy fundamentals and prices expected to appreciate, the IncomePlus Fund’s target portfolio is 75% equity and 25% preferred equity. Going into the COVID-19 pandemic, the IncomePlus Fund’s portfolio was made up of 54% equity, 36% preferred equity and 10% cash. This tactical shift was prescient and provided stability to the Fund’s unit price during the pandemic and enabled us to continue to pay the 6% distribution yield to our investment partners.

Our target portfolio over the next 18 months is closer to 75% preferred equity, 20% equity and 5% cash. This portfolio mix provides capital protection while also allowing us to pay our dividend and grow the unit price of the Fund. This is the prudent strategy as we wait and see how the economy performs over the next six to twelve months, especially after the government subsidies run out. While this will make the Fund slightly less tax-efficient, it will produce far better absolute returns than the alternative. Acquiring assets directly simply to receive the depreciation benefits while ignoring market fundamentals would be irresponsible.

Having the ability to invest in both preferred equity and equity is a unique feature of the IncomePlus Fund and, as we do see improvements in the economy, we will begin to shift the Fund’s portfolio back towards our target portfolio of 75% equity and 25% preferred equity positions. This can actually happen rather quickly as many of our preferred equity positions have rights of first offer, meaning that we can acquire the projects we are lending to in an off-market transaction at up to a 5% discount to current market values. In other words, our preferred equity investments are also a pipeline of future equity opportunities, which is why we only provide preferred equity to highly regarded sponsors who are acquiring or building deals we want to own, because we may someday own them.

Experience Matters

Our experience of acquiring and operating more than 4,000 apartment units enables us to invest in preferred equity in a way that significantly mitigates risk. We scrutinize preferred equity investments in the same way we evaluate equity investments and invest with experienced sponsors who have a history of executing their business plans on time and on budget. We understand how value is created, the qualities of a good sponsor, and have in-house capabilities to take over the property if something goes awry. We have executed dozens of joint ventures and have learned over the years the qualities of a great sponsor and the terms needed to protect us in the event something goes wrong.

The key to generating above market returns during an uncertain real estate market is having a pipeline of quality opportunities and experience in evaluating real estate. Our acquisitions team lives and works in their target markets, establishing on the ground relationships with developers, brokers and property owners. To date, we have never realized a loss on a direct equity investment and focusing on preferred equity investments provides us with another 20% equity cushion, meaning these investments becomes even far less likely to become impaired.

How the IncomePlus Fund’s Preferred Equity Investments Are Faring in Today’s Market

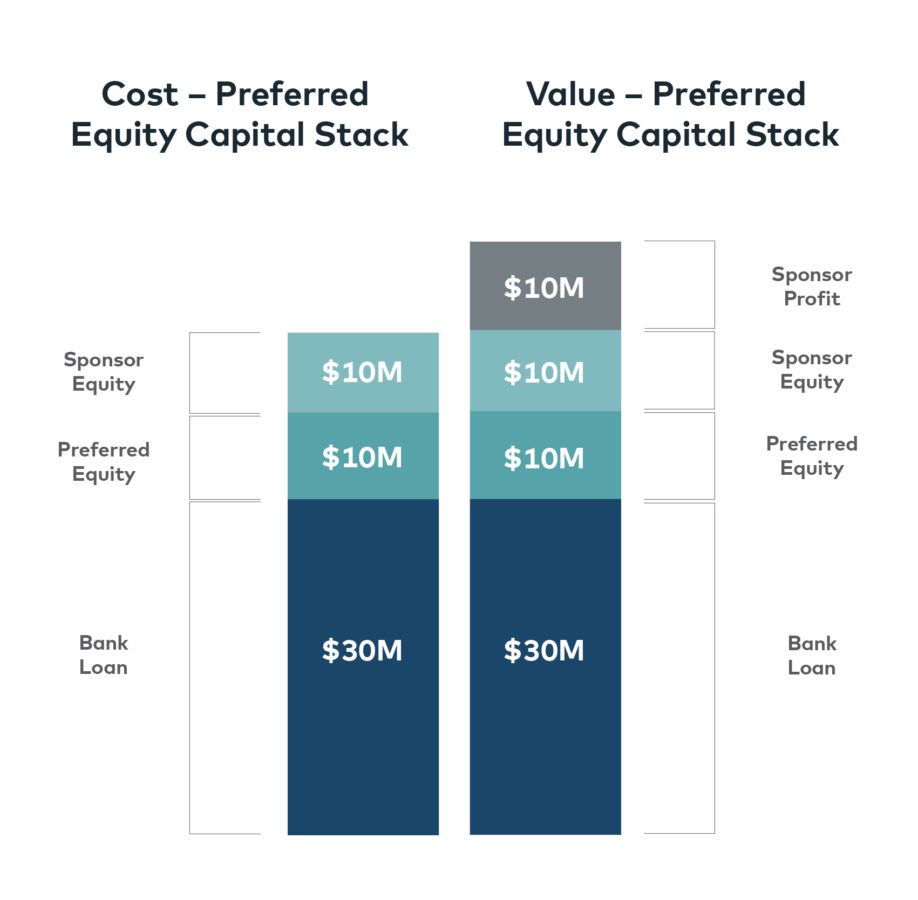

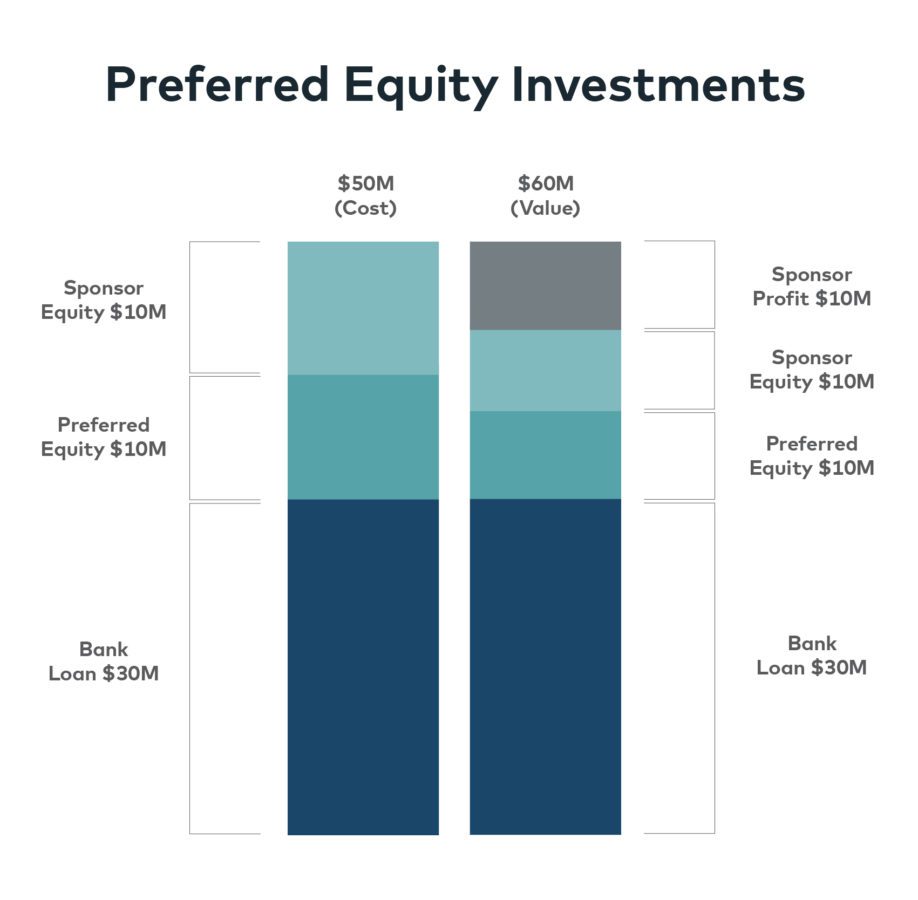

Our preferred equity positions held up well throughout the biggest stress test period of April and May of this year and continue to perform well. There is also a big difference between lending to cost versus value and, while we lend to cost, we also consider the project’s value once completed, and all developers build to make a profit. For example, if a project costs $50 million to build, the projected value upon completion is probably closer to $60 million, leaving the developer with a profit of $10 million, which is the first cushion against loss.

As projects get closer to completion, this profit margin begins to materialize and puts us in an even better position than before. Continuing the $50 million project cost example, if our preferred equity investment was originally made between 60% and 80% of cost, the additional $10 million profit moves our investment to between 50% and 66% of the project’s value. This means that the project’s value can decline 34% before we lose one dollar of our equity. We invest with sponsors who have a history of success and it’s our ability to underwrite and evaluate projects that mitigates risk early on.

April and May certainly eliminated much of the profit margin described above but our preferred equity investments today still have more than a 30% cushion. While the market may have been slightly overheated coming into the pandemic, it was nowhere near a bubble or even close to where the real estate market was in 2008. The 2008 recession was led by real estate because of excess lending in the market and loose standards, but debt and equity providers have behaved responsibly over the past ten years to avoid another real estate bubble scenario. The point is, this year’s recession is likely to be much kinder on real estate than 2008 because we are starting at a place where debt and equity are in equilibrium. It is also highly likely that we will fare far better than real estate sponsors in today’s environment because of our fixed returns and protected positions.

How the IncomePlus Fund’s Equity Investments Are Faring in Today’s Market

The IncomePlus Fund’s assets are performing well in this unprecedented time, with monthly collections above 96% and occupancy stabilizing. Our focus on owning Class A multifamily buildings in growing markets has positioned us to better weather the downturn. Workforce housing, defined as Class B and below, will continue to feel the brunt of the pain as this demographic makes up the majority of the unemployed today. Much of the damage to this end of the economy will be semi-permanent as the restaurant and hotel sectors will take years to recover. We’ve seen this play out in other recessions as well, which is why we have chosen to target a more educated and higher income tenant. These tenants are less susceptible to layoffs, want to protect their credit scores at all costs, have higher disposable incomes and have other sources of income such as savings or family they can tap into to pay rent even if they do lose their job.

We recently wrote down our equity investments in response to the market fundamentals declining, resulting in a reduction in the IncomePlus Fund’s unit price from $10.00 to $9.26. We are confident that these Class A assets located in growing markets will eventually rebound. The IncomePlus Fund’s assets are marked to market every quarter, so while sellers are reluctant to move their price, our equity valuations have been adjusted to reflect the reality of today’s market. This means that existing investors know the true value of their investment and new capital coming into the Fund will be acquiring these same assets at fair market value.

{kind=link}

{kind=link}