When we introduced Growth Fund IV at the beginning of 2022, we were analyzing hundreds of deals to find the best investment opportunities. The Fund’s portfolio of high-quality properties underwent strenuous due diligence before they were acquired, and our analysis accounted for several factors that are now playing out, including cooling rent growth and the increasing likelihood of a recession.

Even as we view the long-term outlook for multifamily investment as positive, remaining complacent and ignoring risk factors during this time is fatal for fund managers. As risk managers, we study a variety of economic scenarios. Below, we have applied those to this Fund and are sharing the results.

We created Growth Fund IV to offer capital growth with a four-year hold. After the initial development period, investors can redeem their interests or remain in the Fund and continue to generate returns. The Fund, whose portfolio includes assets in high-growth markets across six southern U.S. states, closes in March. Our strategy involves investing as a limited partner (LP) and co-general partner (GP) in development opportunities in ground-up developments. That approach offers some of the highest risk-adjusted returns compared with already existing assets.

Properties in Growth Fund IV

The Fund’s portfolio currently includes nine assets:

- Preserve at Star Ranch: Austin, Texas

- Haven at Cool Springs: Franklin, Tenn.

- Haven at Apache: Tempe, Ariz.

- Solace at the Ranch: Colorado Springs, Colo.

- Haven at Lloyd Park: Dallas, Texas

- Auterra Nocatee: Jacksonville, Fla.

- Sutton Place: Jacksonville, Fla.

- 277 Clifton: Atlanta, Ga.

- Sam Furr Road, Charlotte, N.C.

We are navigating pre-development activities on seven of the projects. At 277 Clifton and Solace at the Ranch, construction is progressing. At both those projects, a small markup in value has been made based on construction to date; elsewhere, the project values are held at the cost of acquiring the land sites.

Two deals in this Fund—277 Clifton and Preserve at Star Ranch—represent a newer trend in multifamily construction: build for rent. While this style of multifamily property is generally less expensive to build, rental rates are similar to more vertical properties because residents have amenities such as yards and attached garages.

As well, we plan to close on two new properties later this month: McKinney Falls in Austin, Texas, and Marlowe South Las Vegas. These sites provide compelling margins under stress underwriting and exemplify that good development opportunities, while becoming more limited, are still available via our focused approach to market and site selection.

How We Value the Properties in Growth Fund IV

The valuation of a development project is calculated using future cash flow and the residual value of a completed and fully leased property. As a project progresses through development, investment risk decreases because uncertainty around the timing of project completion and other costs are resolved. One measure of risk we use, the discount rate, or internal rate of return, applied to future cash flow, is highest at the beginning of construction but compresses over time. For more details about how we value the Fund, read our valuation policy.

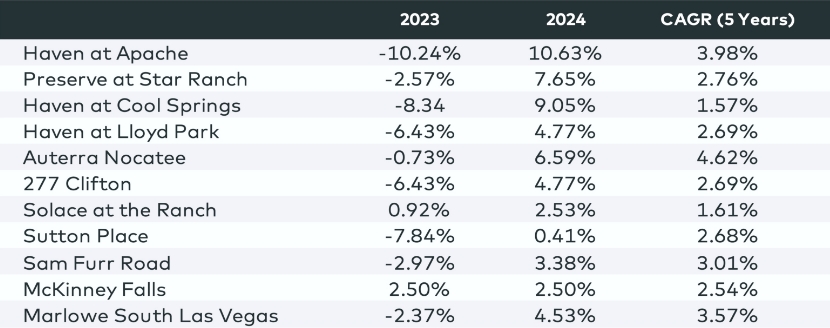

We actively monitor development costs as we underwrite our current projects, including rising interest rates, changing construction and labor costs, capitalization rates that have increased from less than 3.5% to around 4.5%, and the effects of inflation. It also includes cooling rent forecasts—some into negative territory—in the areas in which we invest (see the chart below).

The value of fully leased property relative to the cost to develop is the gross margin. We require our development opportunities to have a minimum gross margin of 30% at the time of underwriting. In some cases, as the economic environment shifts, we may decide that the growing risks no longer make the potential rewards worth the investment.

How We Prepared the Fund for 2023

We have factored two possibilities into our underwriting for the past year on all our Funds, including Growth Fund IV: lower rents and the increasing likelihood of a recession. Both scenarios have been predicted by Origin MultilyticsSM, our proprietary suite of machine-learning models. The life of this Fund extends beyond both of those scenarios, however, and we are investing in markets that we believe will rebound strongly to the five-year growth average. Most of the projects are scheduled to be delivered in late 2025, and we expect the environment to be more favorable than what we are predicting for the next six or 12 months.

The chart below represents the markets in which Growth Fund IV invests, and their weighted average five-year growth, according to Multilytics.

Source: Multilytics

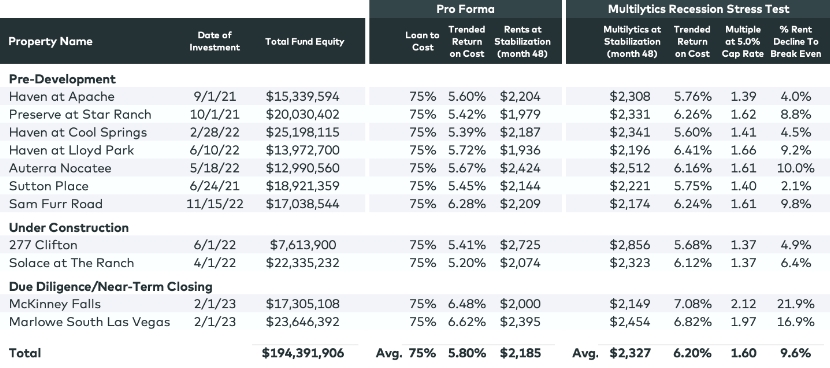

Given uncertainty around final costs for the projects that have not yet begun construction, we stress-test each investment to determine whether it can withstand higher development costs, lower rents and higher cap rates. In the chart below, the original pro forma is on the left with a recession rent forecast on the right.

These investments were capitalized using an average 75% senior debt and underwritten to an average return on cost of 5.80%. The return on cost is calculated by taking the net operating income at stabilization and dividing it by the cost of the project. The difference between the return on cost and prevailing cap rates represents the project’s gross margin. Our minimum gross margin requirement of 30% has helped us greatly in today’s environment as cap rates increased from below 3.5% to around 4.25% to 4.5% in today’s market.

The column on the far right shows the returns using Multilytics’ rent-growth forecasts and a 5.0% cap rate to get a more accurate picture. The “multiple at 5.0% cap rate” column captures the return on our investment using Multilytics’ recession forecasted rents and a 5.0% cap rate. The next column, “% of rent decline to break even,” represents how much these predicted rents would have to decline before our capital is at risk.

Source: Multilytics

In some cases in the chart above, Multilytics’ rents are higher than our underwritten rents. That’s because we employ the concept of margin of safety and present both the forecasted rents and the rents that make the deal work. Forecasted rents always are the ceiling, but if the project can work with lower rents, that is how it is approved. The underwritten rents above represent the approved rents. In most cases, the forecasted rents were much higher.

Working with a Changing Economic Scenario

As we refine our cost expectations, some projects still in pre-development will no longer meet our margin requirements. In those instances, we may limit the Fund’s investment to a GP interest or an alternative structure to improve returns and limit risk exposure. Or we may find another approach that allows the project to meet required returns. The chart above reflects investing the majority of LP equity in the projects. For example, the current projected return on cost for Haven at Cool Springs does not meet our established margin requirements, so we are refining costs and analyzing other capitalization scenarios to improve returns and manage risk.

If we move forward on a deal, it means that even in these changing market conditions, it meets our cost of capital. Our goal in painting a realistic picture for investors about the short-term pains is to underline our long-term optimism in this Fund. Our co-founders are aligned with our investors in Growth Fund IV because we believe that picture of future growth is positive—that we are in resilient markets and high-potential deals, in areas that will experience strong demand now and in the future.