Where and When Will Distress Hit in Commercial Real Estate?

Headlines have been portending stress in the real estate capital markets since regional banking issues surfaced over the past few months. But outside of the iceberg that is the (suburban) office market, red lights do not appear to be flashing yet. When will this distress occur in commercial real estate, and which sectors will be hardest hit? The answer is exceptionally complex: Influences on the real estate capital marketplace are varied and nuanced, and include underlying fundamentals by asset class, asset quality and location. All those work in concert with macro liquidity issues such as desirability and the availability of debt and equity capital.

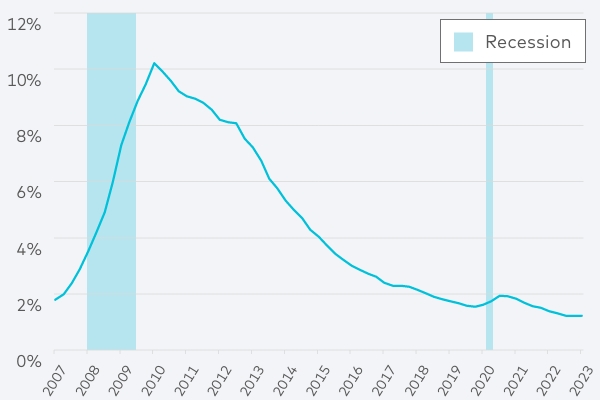

Historical context can provide some clues for when and where distress may surface. Even those who endured the Global Financial Crisis (GFC) often forget how long it took for distress to appear in the broader market. Bear Stearns collapsed in late 1Q 2008, and Lehman followed in late 3Q 2008. According to the St. Louis Federal Reserve, delinquency rates on commercial bank loans secured by commercial real estate were 3.5% in 1Q 2008. That increased to 4.9% by 3Q 2008 and did not peak, at 10.2%, until 1Q 2010, a full two years after Bear Stearns’ collapse. As of 1Q 2023, the delinquency rate was 1.2%—lower than any period leading up to the GFC, including the 1.3% recorded in 4Q 2004.

Delinquency Rate on Loans Secured by Real Estate,

All Commercial Banks

Source: St. Louis Federal Reserve

Because challenging underlying fundamentals and liquidity issues manifest in either delinquent or unrepaid loans, loan delinquencies provide one of the best barometers for distress. Using this information as a compass, it is likely that distress will not fully emerge in the marketplace for at least a few more quarters after delinquency rates begin to spike.

Anecdotally, some of the best buying opportunities in the years after the GFC—at least at any sort of scale—did not fully manifest until late 2011 and early 2012. It took three to four years for most lenders to work through their delinquency and default issues and return as an active provider of debt capital. Many of the transactions in the early quarters after the Lehman collapse were done on an all-cash basis due to lack of available leverage in the system. The GFC prompted Dodd-Frank reforms of the banking system that are keeping most lenders today in far better fiscal shape to weather a commercial real estate storm. So, if and when true distress emerges, it’s unlikely that it will take three or four years for debt capital to be readily available to finance acquisitions and developments.

Over the past few quarters, we have seen a significant pullback in new originations from commercial banks, as discussed in a prior Market Monitor. More recently, this has been accelerating due to potential reforms to Dodd-Frank regulations to establish further guardrails at smaller banking institutions. These reforms attempt to prevent failures similar to those of Silicon Valley Bank and First Republic Bank earlier this year.

We have observed a number of debt funds helping to fill the void, but borrowing rates are not exactly cheap—often priced at 500 or more basis points over SOFR, which translates to an all-in interest rate north of 10%. If the Fed doesn’t lower short-term interest rates—on Wednesday it hit pause on increases, at least—and if our projections are accurate and rents begin to decline over the next 12 months, additional stress could be placed on borrowers of these products upon refinance or sale. However, if these events were to play out, this distress would not be realized for three years or more.

Given the macro demand fundamentals supporting rental housing in the United States, especially where much of the new supply is being delivered, it is unlikely that both rents and the debt capital markets will remain depressed for an extended period. As such, it appears likely that distress within the multifamily market at any sort of scale is likely several quarters away. And the level of distress is unlikely to be as severe and long-lasting as the period after the GFC.

While distress in the office sector remains worth watching, within multifamily, borrowers experiencing varying levels of distress still have options with debt and equity sources. Real distress will not emerge until those financing options dry up and delinquency rates increase.