Why Haven’t Cap Rates Exploded?

Dave Welk, Managing Director of Acquisitions

One of the most discussed market dynamics lately is the concept of negative leverage, which arises when a property’s borrowing rate exceeds its cap rate. Given the significant increase in underlying interest rates for fixed- and floating-rate mortgages—now approaching 5.75% and 7.50%, respectively—various market participants are perplexed that underlying cap rates have not expanded by a similar amount.

Cap rates for institutional Class A assets seem to be settling in the mid-4% range in the Sunbelt and Mountain regions, implying that investors are taking on negative leverage to the tune of 2% to 3%, which is historically high.

Is further expansion on the horizon? Several factors could keep this from happening. One is that buyers are betting that multifamily rents, which have increased 22% nationally and more than 40% in several Sunbelt markets since March 2020, will continue to rise. Another is the expectation by many market participants that if Fed moves trigger a recession, a period of quantitative easing would ensue, resulting in lower interest rates. If that happens, a positive leverage environment would return.

Because many multifamily investors, especially in the Class A institutional segment, are long-term holders, they can look past periods of market dislocation. Many investors believe that long-term terminal, or exit, cap rates eventually will return to a more normal spread above the 10-year U.S. Treasury yield. Except for 2005-08, they have hovered closer to a 1.5% to 2.0% premium above the corresponding Treasury yield.

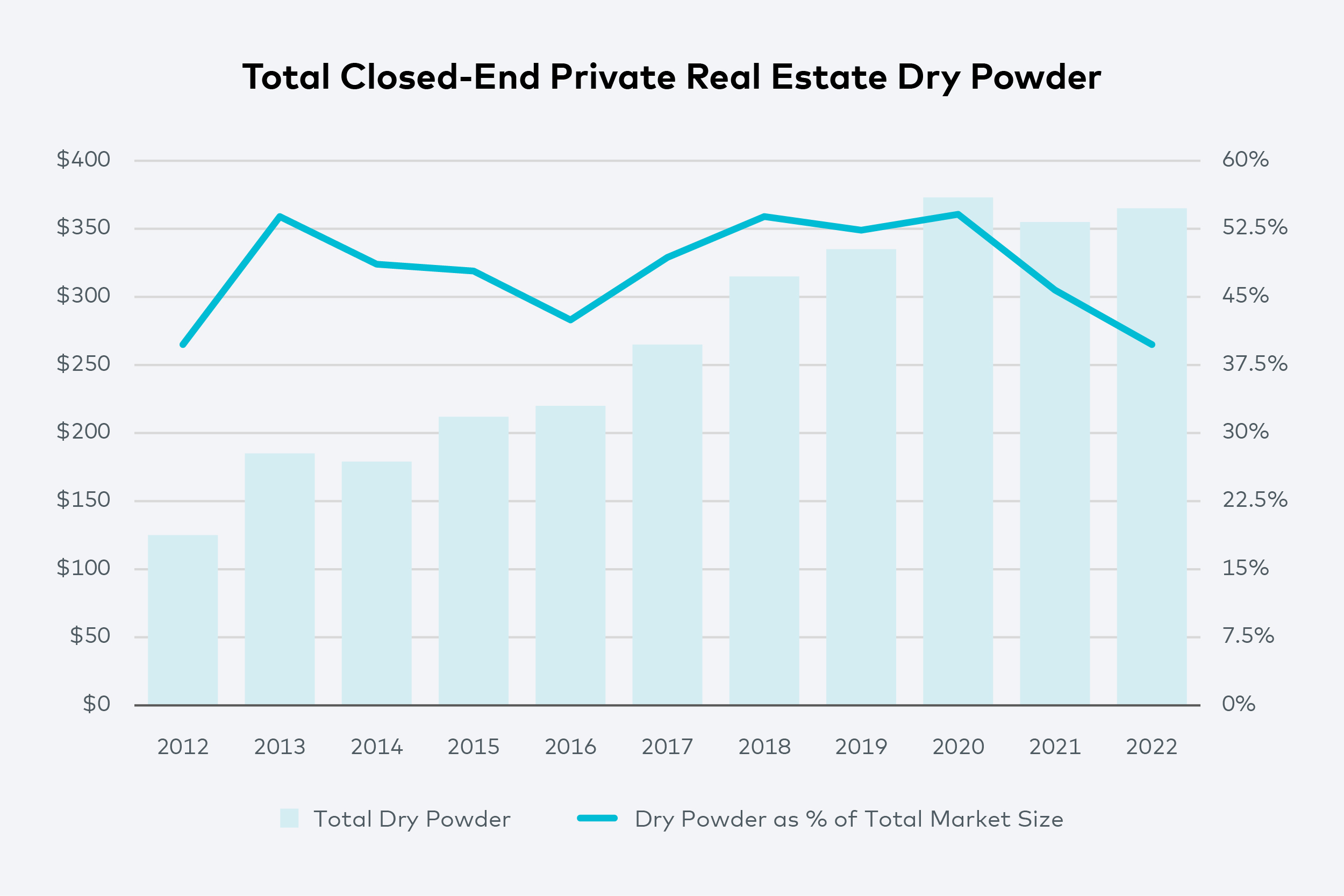

The last two factors keeping cap rate expansion at bay are related to capital markets on both the equity and debt side of the ledger. An estimated $350 billion in capital has been raised by closed-end private equity vehicles targeting U.S. commercial real estate—roughly 38% of the entire investable market (see chart). Much of this is targeted at value-add and opportunistic investments and has been sitting on the sidelines waiting for signals of significant value declines.

Sources: Preqin and NCREIF, via CBRE

But with that much liquidity in the marketplace, there is a somewhat narrow limit on how far values will fall before reaching price stability. Prior periods of dislocation resulted from overleveraging and untimely loan maturities. Currently, 88% of outstanding multifamily mortgage debt has been originated by government agencies (Freddie Mac, Fannie Mae, HUD), banks and life companies. All have tightened underwriting standards since the Great Recession. As a percentage of the overall debt market, only a minority were financed with high-leverage, short-term bridge financing, which significantly limits the leverage risks that plagued previous cycles.

It appears that a significant majority of owners of private multifamily real estate took advantage of the low fixed-rate environment over the past 24 months. With these owners benefiting from both historically low fixed-rate debt and historically high rent growth, the distress in the market from 2008 to 2010—the most recent period of significant cap rate expansion—may not occur. If that’s true, instead of the cap rate explosion anticipated by $350 billion of dry powder, investors may have to settle for just some air being let out of the balloon.

Interest Rate Moves Tell the Story

Tom Briney, Managing Director of Acquisitions

Over the past few weeks, there has been a peculiar movement in interest rates. The headlines of early November were all about the Federal Reserve Bank increasing interest rates to the highest level since 2008 in an attempt to slow the rate of inflation. However, one observation has been noticeably absent: The borrowing costs for longer–dated loans—across Freddie Mac’s 10-year fixed rate, home mortgages and life company loans—have been holding steady, and in some cases, falling slightly from their peaks. The diverging rates are telling a story about today’s economic picture compared to the economic picture expected in the future.

On Nov. 2, the Fed increased the high end of the overnight lending rate, or Federal Funds Rate, to 4.00% from 3.25%, a move widely anticipated by capital market participants. However, since Oct. 24, the upper–limit borrowing cost for a 10-year Freddie Mac fixed-rate loan for an apartment community has decreased to 6.19% from 6.25%. How can one interest rate increase dramatically while another holds steady? The answer: Expectations.

Sources: Federal Reserve Bank of New York, Freddie Mac

The Fed Funds Rate is used for overnight lending among financial institutions, generally banks. An increase in this rate immediately impacts how much money is available for other groups to borrow, and the rate at which they can borrow. This flow of money, called M2, directly impacts U.S. economic growth. More money equals more growth, and less money equals less growth. As the Fed increases rates, there’s less money in the system, the expectation for future economic growth decreases—and longer–dated rates confirm that expectation.

We’re using the modest decrease in the Freddie Mac 10-year fixed rate to illustrate this because Freddie Mac is a big part of Origin’s business. The tightening of money flows by the Fed is driving expectations for slowing economic growth, or possibly contraction—and a recession—over time. In that case, the Fed will be forced to reduce rates, loosening money flows and spurring economic growth once again. The 10-year rates are the predictor of this future economic loosening, and the more disconnected they become from the Fed Funds Rate movement, the more conviction the market is demonstrating that the economy will contract. It’s very important to watch both the Fed Funds Rate and the 10-year rates, but it’s even more important to watch the relationship between those rates—that’s where the real story is told.