There’s an age-old question that many investors ask themselves and their advisors: Is now a good time to invest?

What history has taught us is that for long-term wealth creation, time in the market is far more important than timing the market. If you’re a financial advisor, it’s likely that this response is not new to you. That being said, investing with good market timing, whether it’s by chance or done strategically, can also impact the return on investment you achieve over the long term. That’s true in multifamily investment performance as well.

Various leading indicators and fundamental trends have emerged that point to strong multifamily investment performance over the coming years. In this article, we’ll walk through each of these trends which can be utilized to help you determine your future investment plans.

Subscribe

Subscribe to receive the latest articles about fund updates, industry news and market trends.

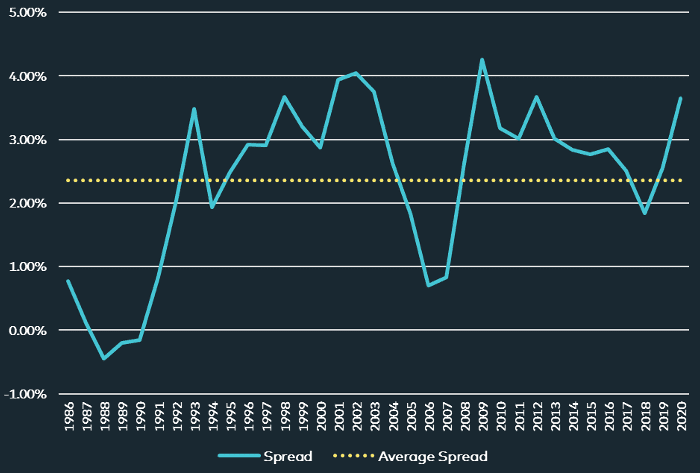

1. Spread Between Multifamily Cap Rates and Borrowing Costs

As history indicates, a large spread between median cap rates of stabilized multifamily properties and the interest rate of the 10-year U.S. treasury bond is most often an excellent leading indicator of strong future performance of multifamily properties.

Multifamily Cap Rate Spend Over 10-Year U.S. Treasury Yield

*Average annual spread vs. 10 Year Treasury (1986-2020) Source: NCREIF Property Index (Apartments)

While we know the rule of thumb that says past performance is not always indicative of future results, take a look at three of the highest peaks prior to 2020, which are 1993, 2002 and 2009. According to the NCREIF Apartment Property Index, in the five-year period following each of these peak years, private multifamily real estate produced an average annual return of 17%.

The cap rate spread today (i.e. in 2020) is at a 10-year high.

2. Supply and Demand

In the 10 years prior to 2017, the U.S. renter population grew by 19.6 million people. The National Apartment Association and National Multifamily Housing Council recently projected that, based on the forecasted growth of the renting population, the U.S. will need to build 328,000 new apartment homes each year to meet renter demand. To put this into perspective, the average annual amount of new multifamily units that were built over the last 10 years has been only 239,000.

Annual New Supply Required to Keep up with Forecasted Demand Growth

*National Multifamily Housing Council & National Apartment Association, Vision 2030.

The U.S. Census Bureau also reports that the national rental vacancy rate compressed even further in 2019 and is now at 6.8%, the lowest level since the mid-1980s. According to RealPage, vacancy rates in most U.S. markets posted year-over-year declines of 0.7% as of Q3 2019.

With vacancy rates at generational lows, multifamily rent gains are likely to continue outpacing general inflation in the U.S. for quite some time. A widely used measure of inflation, the Consumer Price Index (CPI), most recently posted inflation at 2.3% over the past year, which compares with 3.7% year-over-year rent growth that multifamily properties achieved on average in 2019.

A longstanding principal of microeconomics says that the price or value of an asset is typically dictated largely by the level of demand for the asset relative to the available supply of it. All else equal, if incremental renter demand proves to exceed incremental new supply of multifamily units over the next 10 years, then this is likely to come with price appreciation.

But who and what are really driving these supply and demand fundamentals?

3. Evolving Renter Demographics

When we break down the population of the U.S. into generational groups, the largest working generation today is those between ages 18 – 34, more commonly known as the Millennials and Gen Z. This age group also happens to make up the largest portion of the renting population in the U.S. today, at roughly 39 million people. The total population of renters in the U.S. today, now over 100 million people, represents an all-time high and is expected to continue growing and notching new all-time highs almost every year. However, this age group is not the only demographic that will influence renting and multifamily demand fundamentals going forward.

Since general population growth is another key macro driver of multifamily investment performance, it’s important to understand which demographics are likely to continue driving much of our country’s population growth. Per the National Apartment Association, it’s predicted that roughly half of the population growth in the U.S. over the next 10 years will not come organically. Rather, half of the predicted growth is expected to come from net new migration to the U.S. While roughly 35% of native-born citizens in the U.S. currently choose to rent instead of own a home, more than 70% of immigrants who moved to the U.S. in the past five to ten years rent. As U.S. population growth continues to be driven more and more by immigration, the overall percentage of renters could continue to grow as well.

We are also seeing a growing presence of high-income renters. According to The National Multifamily Housing Council, renter households with incomes of $75,000 or more made up almost 25% of the total renting population in 2019, representing a surge in the growth of this high-income cohort. On average from 1990 – 2010, this same cohort made up only 18% of the total renting population. All else equal, continued growth in the high-income renter cohort will bode well for rent growth over the longer-term.

% of Apartment Households Earning Greater Than $75,000/Year

*NMHC tabulations of 2018 Current Population Survey, Annual Social and Economic Supplement microdata, US Census Bureau. Updated 2019.

As renting becomes more and more of a lifestyle choice, and not just an economic one, apartment demand will be driven by all age and income cohorts.

Conclusion

While time spent in the market can outweigh an investor’s relative market timing when investing for the long-term, layering on good market timing can also be materially accretive to your clients’ return on investment and we have no information today that leads us to believe that the multifamily market won’t continue to grow. At Origin, our investment strategy’s primary focus is in the multifamily asset class in some of the fastest-growing U.S. markets. Click here to learn more about how Origin’s passive multifamily investment solutions can be a valuable addition to your core portfolio allocation strategy.