One major obstacle that almost all advisors face in the current market environment is finding healthy sources of income for their clients’ portfolios while not exposing those clients to outsized levels of risk. The baby boomer generation has caused a major demographic shift in the United States over the last 80 years. As this enlarged generation grew up, entered the workforce, bought homes, raised families, and grew their careers, the effects were seen all over the U.S. economy – everything from the housing and stock markets to certain sales trends (cars, bicycles, microwaves) soared. We now find ourselves at the point where boomers have graduated from the accumulation phase of their life to the distribution phase, and they are in need of income from the wealth they built. With such a demand for income, along with many other factors such as monetary policy, interest rates have continued to find new bottoms. It has become very slim pickings at a time when portfolio income is needed more than ever before.

In this article, we’ll explore the challenges that come with some of the commonly used methods of sourcing income. How can advisors find ways to accommodate baby boomers’ need for income, all while keeping risk levels at bay so that they don’t hinder their clients’ financial plans, and in turn, their position as a fiduciary? On top of that, how do they do this in an environment of rapid change? We’ll take a deeper look at the current market landscape and the outlook moving forward to help us answer these questions.

Looking back over the last several decades, investments in bonds fared very well in portfolios. Bonds served three important purposes: they paid income, they provided capital preservation with less perceived risk than equities, and they offered correlation benefits through asset allocation, which in turn helped enhance risk-adjusted returns. However, we now find that all three of these benefits have greatly diminished. Let’s take a look at each of these challenges in depth.

1. Income is scarcer than ever

The chart below helps highlight how low interest rates are today when compared to the last 50 years. As of July 31th, 2020, the U.S. 10 Year Treasury Rate sits at 0.55%. Compare this to 15.84% in 1981 when boomers were in the heart of accumulation phase and the demand for money was fierce. Collecting that level of income in an essentially risk-free U.S. government bond made the retirement game much easier back then.

While low interest rates have been a topic of discussion for several years, it has only become more pronounced this year with the market uncertainty surrounding COVID-19. As investors seek safe-haven assets, the 10 Year Treasury rate has fallen another 70% from the 1.88% level it sat at on January 1st.

2. Fixed income presents new risks

With various risks now heightened, fixed income does not offer the security of capital preservation that it once did. Let’s break down the two primary types of risk:

Duration risk: This is the risk of increasing interest rates or a steepening yield curve hurting the principal values of bond investments. To put this risk into the context of today’s market, if the 10-year Treasury rate were to increase to where it was as recently as January 1st of this year, it would experience a 220% increase from the current level. A retrace in rates to where they were just seven months ago would hurt fixed income investments by as much as 70%. Unfortunately, the safer credit investments, such as Treasuries or investment grade fixed income, tend to carry the most duration risk.

Credit risk: This is the risk of bond issuers defaulting. This risk becomes more pronounced in a recessionary environment. Corporate bankruptcies are currently on the rise, and there is still great uncertainty with the pandemic looking forward. How COVID-19 affects demand in certain industries, employment rates, and household income, will determine how drastically the corporate environment could suffer. These factors paint a portrait of an environment that may not be reflected in fixed income risk premiums.

3. Correlations between stocks and bonds are unpredictable

The third perceived benefit of fixed income that we mentioned, low correlation to equities, is very questionable as well. With many new factors at play such as increased Fed intervention, fixed income is not showing the allocation benefits that it once did as correlations between stocks and bonds have converged.

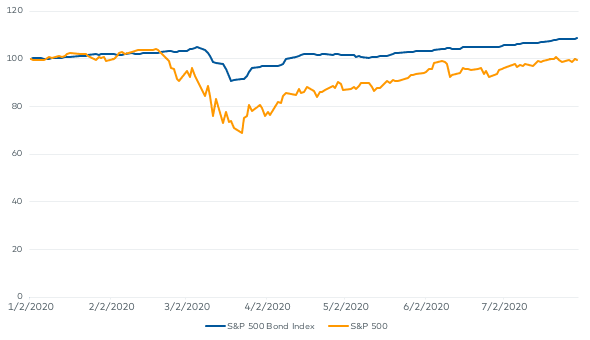

Economic downturns are the times when low correlations among asset classes are most important. (We need assets that will “zig” when stocks decide to “zag.”) The chart below shows how the S&P 500 and the S&P Bond Index have performed through the volatility we experienced this year. When the S&P 500 experienced a downturn of over 34% from February 19th to March 23rd, bonds sold off as well. Investors fled to cash, and the U.S. Dollar appreciated rather than bond values. Since then, both have retraced in parallel fashion.

2020 Performance: S&P 500 vs. S&P Bond Index

Many risk management tools use backward-looking data to figure out how to best allocate among various asset classes moving forward. However, this is a time of great uncertainty, and demographic shifts remain an ongoing catalyst for change. This could present problems at times when risk management is needed most.

Other Sources of Income

Today’s combination of low interest rates, heightened risk and more complicated risk management makes for a tough environment for traditional fixed income investing. Below are some alternative sources of income in the marketplace that we have seen investors using, along with a few things to heed attention to when considering them:

Stock dividends: While dividend-paying equities offer both income and the potential for appreciation, they have very high risk levels with the market near all-time highs. The dividend yield of S&P 500 is also very low, only 1.93% as of July 29. When looking for income, this does not make for a risk-efficient way of executing, especially as stocks offer no correlation benefits.

Preferred stock: As opposed to the general stock market, preferred equities may offer yields above 5%. However, they can also create concentrated risks, as the asset class is highly focused on banking and financials. In an economic downturn, these industries experience great stress. Preferred equities experienced equity-like losses in March of this year when COVID-19 hit.

High-Yield Corporate Bonds: These bonds are very prone to defaults in a recession and as mentioned, we have already seen an uptick in defaults. They also have a strong correlation to equities.

High-Yield Municipal Bonds: Municipals offer tax-advantaged income, which helps the after-tax income figure an investor receives. Income levels of more than 5% can offer tax-equivalent yields of near 8%. They may also provide correlation benefits when compared to other fixed income asset classes. However, as with other fixed income, they will experience duration risk, and they will experience credit risk based on the performance of the governments or projects they are backed by, all of which are susceptible to the current economic uncertainty.

MLPs: MLPs have become attractive to yield-thirsty investors over the years, as they can provide yields north of 7%. Unfortunately, investors must stomach a great deal of volatility to partake, along with a high risk of defaults. Looking back to earlier this year, the Allerian MLP Index fell over 69% from January 15 to March 18. MLPs are highly concentrated in the energy industry, which has suffered greatly from adverse supply/demand dynamics this year.

How We Invest at Origin

Every investor is different as far as their goals, their time horizon, their risk appetite, and countless other factors. For investors that have a time horizon of over ten years, a window opens to opportunities that allow them to take on more risk in exchange for potentially higher returns and greater sources of income. However, a longer time horizon also creates uncertainty as far as what our world looks like several years out. For that reason, even many longer-term sources of income are still hard to justify.

At Origin, risk management is inherent in everything we do. We are currently focused on multifamily properties in the markets where we see positive economic trends that we anticipate to progress for many years to come. The Origin Income Plus Fund offers a current distribution rate of 6.4%, and we’ve never missed or reduced our monthly distribution. The Fund also has a target of an additional 3-5% per year of capital appreciation. Additionally, we can write off depreciation and interest expenses on our properties which creates tax efficiency, one of the great benefits of direct real estate investing. A tax-free distribution of 6.4% would equate to a tax-equivalent yield north of 9% for investors in top tax brackets.

Strong Risk-Adjusted Returns

While many economic sectors face great uncertainty right now, people will always need a place to live. As a result, multifamily real estate fared well when most other investments experienced weakness earlier this year. As you can see, the multifamily asset class has provided significantly higher return with significantly less risk than other real estate asset classes over time.

Bubble sizes represent the sharpe-ratio for each property type—a measure of excess return, above the risk-free rate, per unit of risk for a given property type.*Represents the average annual risk-adjusted return over each 10-year period from 1990 to 2020. Data source: national council of real estate investment fiduciaries (NCREIF).

Multifamily housing has also shown low correlations compared to the broad stock and bond markets. In a world where correlations are less predictable, this asset allocation’s benefits can be very valuable.

20 Year Asset Correlation Numbers

| Russell 3000 | Barclay’s Aggregate Bond Index |

FTSE Nareit All Equity REITs Index |

|

|---|---|---|---|

| NPI-Apartments* | 0.17 | -0.18 | 0.28 |

Not all multifamily is created equal

Our Income Plus Fund focuses on Class A Multifamily Value-add projects. Rather than development projects that have more uncertainty from start to finish, the Fund purchases projects that are already leased up and with tenants that we classify as “renters by choice.” This means that our tenants have the financial potential to be homeowners, but they are choosing to rent for various reasons. In a recession, these renters will be least likely to forgo their rental payments, which helps us maintain a consistent monthly distribution and a stable NAV even in tough times.

Tactical management across the capital stack

An important feature of how our team manages the Income Plus Fund is that we invest across the real estate capital stack. This means that we pursue opportunities in preferred equity or debt, where we are the lender. This significantly lowers portfolio risk while maintaining strong income. Preferred equity can offer a 30% cushion of protection against falling values, while still proving returns of 10-13%. Three of our portfolio’s five holdings are currently in preferred deals, a key factor in our lack of volatility this year. We will always pursue the benefits that make the most sense for our investors in any given market environment.

Conclusion

In a changing environment with risks we have not seen before, paired with an ever-increasing percentage of advisors’ client base needing yield, income investing has become an industry-wide challenge. At Origin, we believe that real estate, particularly multifamily housing, is an important sleeve in any long-term investment strategy, made even more integral in securing income and mitigating risk in a time of unprecedented uncertainty.